Just a last reminder that prices for all Quantifiable Edges gold and silver subscriptions will be rising after today. Sign up for a subscription today if you want to permanently lock in your rate at a lower cost. Feel free to contact us if you have any questions.

While the Fed is ignoring inflation, one place that prices will soon be going up is at Quantifiable Edges. After Sunday, October 3rd, all gold and silver subscriptions with see a price increase. But you can lock in your prices at the current level by signing up for a subscription before then. I have rarely raised prices in the past, and have always grandfathered in current subscribers at their initial price level. (Yes, I still have a subscriber paying the original annual subscription fee from 2008-09.)

Of course the Bureau of Labor Statistics, who calculates CPI, would likely say that a Quantifiable Edges Gold Subscription has seen a price decline after making their “quality adjustments”. New features over the years have continued to add value. This includes the popular QE Seasonality Calendars and the code (Tradestation, Excel, and Amibroker) that goes along with the Calendars for backtesting, which was released near the beginning of this year.

So whether you prefer to pay monthly or annually, you can lock in the current rates now, before they go up this weekend. Feel free to reach out with any questions. Here is our Gold Subscription page and our Silver Subscription page.

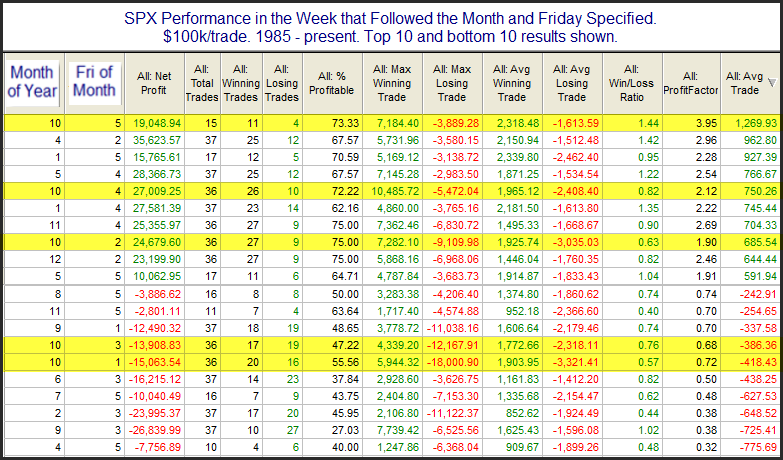

October is a month that is known for volatility. And that is a well-earned reputation. Crashes in 1929, 1987, and 2008 all occurred in October. But volatility cuts both ways. If you break the year down into 1-week periods, October also contains some of the strongest seasonal edges of the year. There have been some very big swings in October, and not just by Mr. October.

Breaking the year down by week is something I have done numerous times over the years, and it has provided some interesting insights. The table below shows stats back to 1985. I chose 1985 as the start date because SPX options trading began in 1984, so 1985 is the 1st full year where there was an options expiration schedule. Action on and around options expiration, which occurs on the 3rd Friday of each month, seems to generate some seasonal tendencies. So this study encompasses the full range of time that SPX options have been in existence.

You’ll note that the highlighted weeks are the October weeks. It’s amazing that all 5 potential weeks in October are included in either the Best 10 or the Worst 10 weeks of the year. Weeks are ranked based on Avg Trade (last column).

Weeks following the 1st and 3rd Friday in October have been among the worst on average. I’ll also note that the 2 largest “max losing trades” occurred following the 1st and 3rd Friday in October. They were a 12% and an 18% drop.

Weeks following the 2nd, 4th, and 5th Fridays in October made up 3 of the best 10 weeks of the year on average. And they show three of the largest winners as well, with 7.2%, 7.3% and 10.5% max gains.

As I said, October can be volatile. There could easily be some strong moves up and down throughout the month, and traders may want to keep this in mind for position sizing, or if they are making volatility trades.

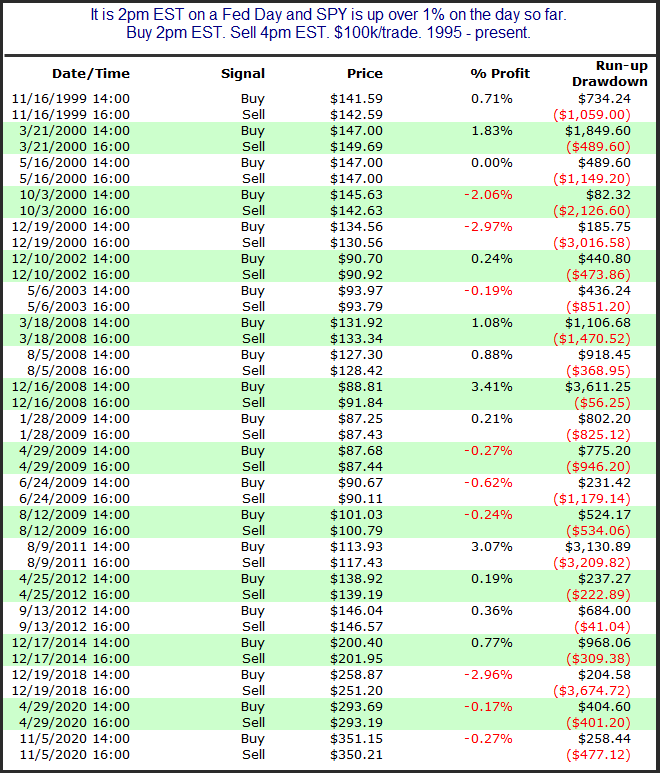

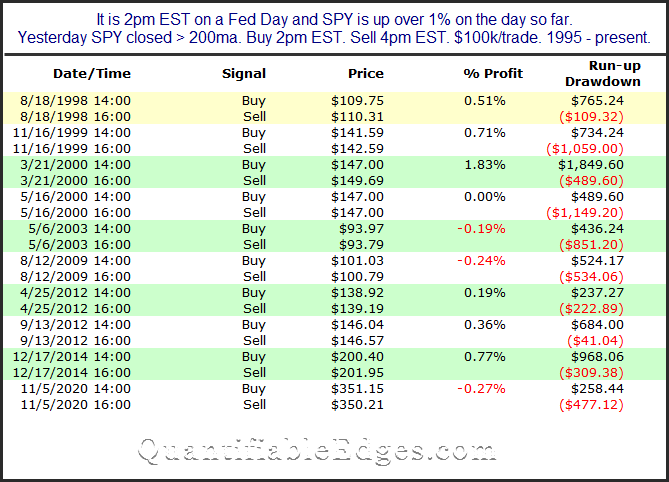

The market is off to a strong start to the day, with SPX up over 1% at around noon EST. I decided to look back at all times the market was up at least 1% at 2pm on a Fed Day (the typical time for a statement release). Below is the full list of instances and their 2pm – 4pm EST performance to finish the day.

Returns here are mixed, and don’t suggest a strong directional edge either way. There have been some strong moves in both directions after the announcement. I also filtered for times SPY was in a long-term uptrend (above its 200-day moving average). Those results are below.

These results are a bit more encouraging. Six of the ten instances saw further gains. One finished flat vs 2pm. The other three saw only mild declines, but still finished the day overall positive. Should be an interesting finish to the day. The good start seems to be a potential positive.

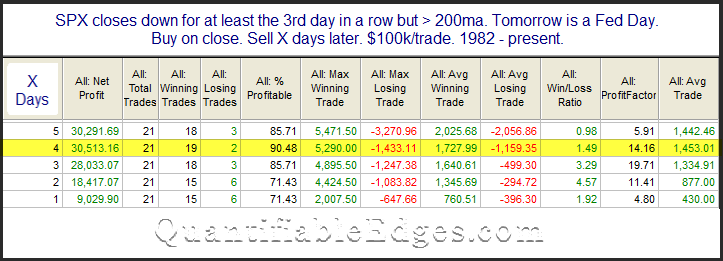

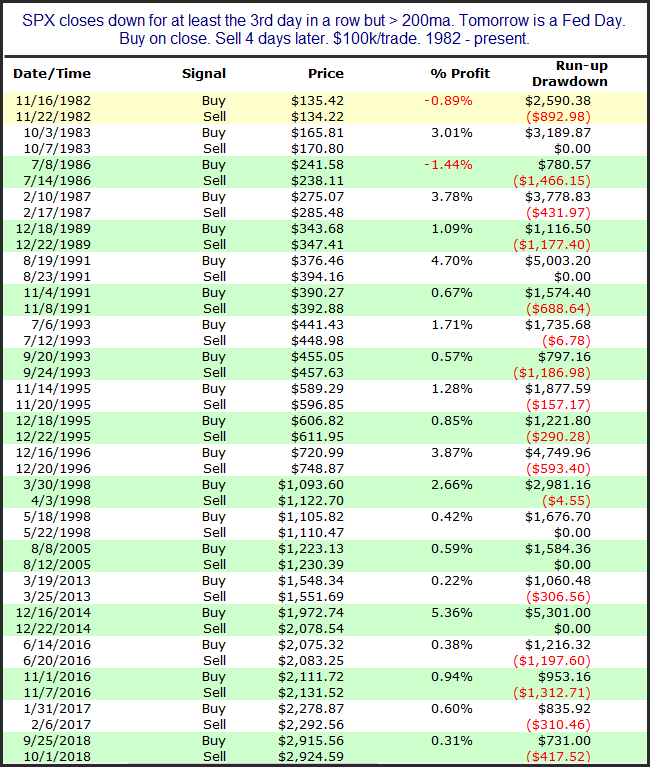

Fed Days often generate compelling studies to consider and share in the nightly subscriber letter. I have also covered them in the blog many times over the years. A Fed Day is one of eight days per year that the Federal Reserve concludes one of their scheduled meetings and makes a policy announcement. Wednesday is a Fed Day. Historically, Fed Days have had a bullish inclination. That inclination has been even stronger when there has been selling heading into the Fed Day. The study below examines other times that SPX was in a long-term uptrend, but closed down for at least the third day in a row going into the Fed Day.

These are some very encouraging numbers for the bulls. Below is the list of instances.

The setup has certainly been potent over a long period of time. There has not been a loser for the 4-day holding period since 1986. And every instance back to 1982 has closed higher than the entry price at some point in the next 4 days. Of course anything can happen when it comes to the market, but evidence here suggests a substantial upside edge over the next few days.

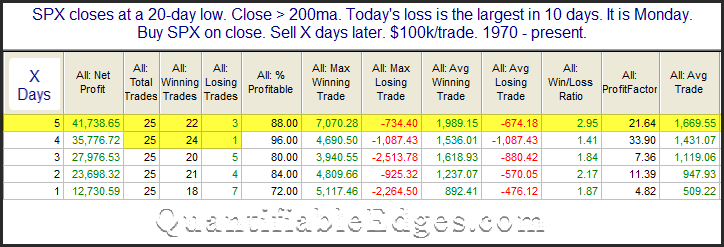

Many studies identified by the Quantifnder Monday afternoon showed the strong selling and closing lows to be potentially bullish. And Turnaround Tuesday is typically the best day for a bounce to begin. The study below considered the long-term uptrend, intermediate-term low, and strong selling on Monday.

The only instance that did not close higher 4 days later was the one that triggered on 2/5/18. But it did close higher on day 5. In fact the last 18 instances all closed higher 5 days later. The last 5-day loser was in 1981. There are certainly dangers right now, but this suggests a high probability of a bounce in the coming days.

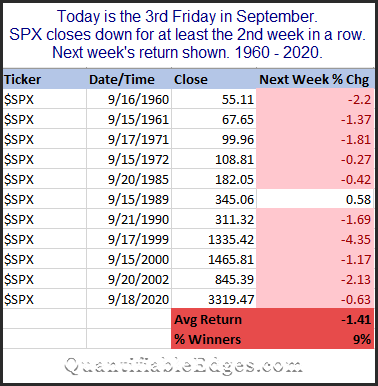

For years I have written about the “weakest week”. It is the week following the 3rd Friday in September, and it has been the worst week seasonally when measured over many time periods. I wrote about it in some detail recently in ProActive Advisor Magazine.

But this year we are seeing two weeks of selling before we even get to the “Weakest Week”. So did the weakness arrive early this year, and are we more likely to see a move higher next week because of this? This is something I examined last year. Below I have updated the table showing all instances of 2 week selloffs heading into the Weakest Week, and then the Weakest Week return.

There have only been 11 instances. But 10 of 11 saw further selling in the Weakest Week. The lone winner (1989) only managed a 0.58% return. The average week of the sample saw a 1.41% loss. This is not encouraging for people hoping for a bounce next week.

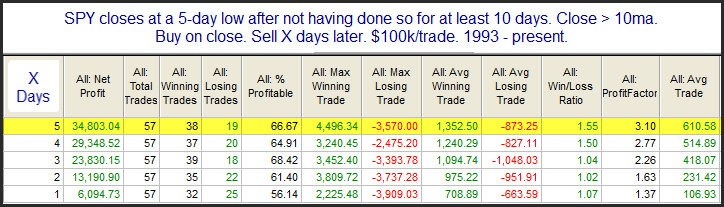

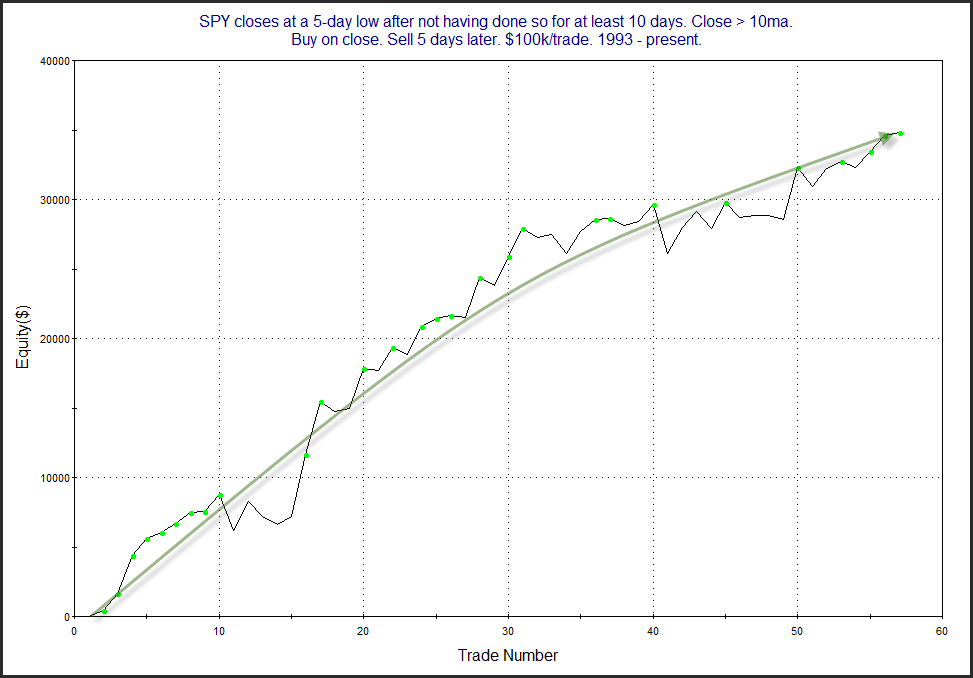

Tuesday’s action caused SPY to close in an interesting position. Traders could look at the chart and say it is “short-term oversold” due to the fact that it closed at a 5-day low. They might also say it is “short-term overbought” since it closed above its 10-day moving average. I have found that edges often arise when something is short-term overdone in one timeframe, but overdone in another direction in another timeframe. The study below looks at the current discrepancy.

Results here suggest a solid edge over the next 1-5 days. Below is the 5-day profit curve.

The strong and persistent upslope is impressive, and serves as some confirmation of the bullish edge suggested by the numbers. Traders may want to keep this in mind when setting their bias for the next few days.

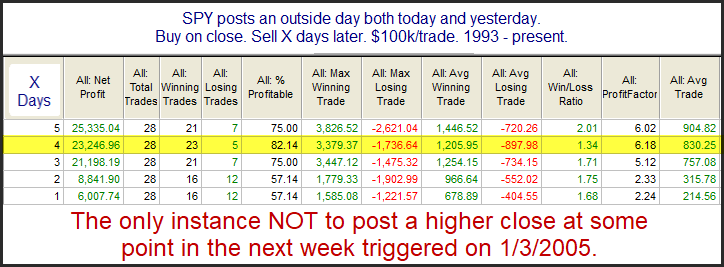

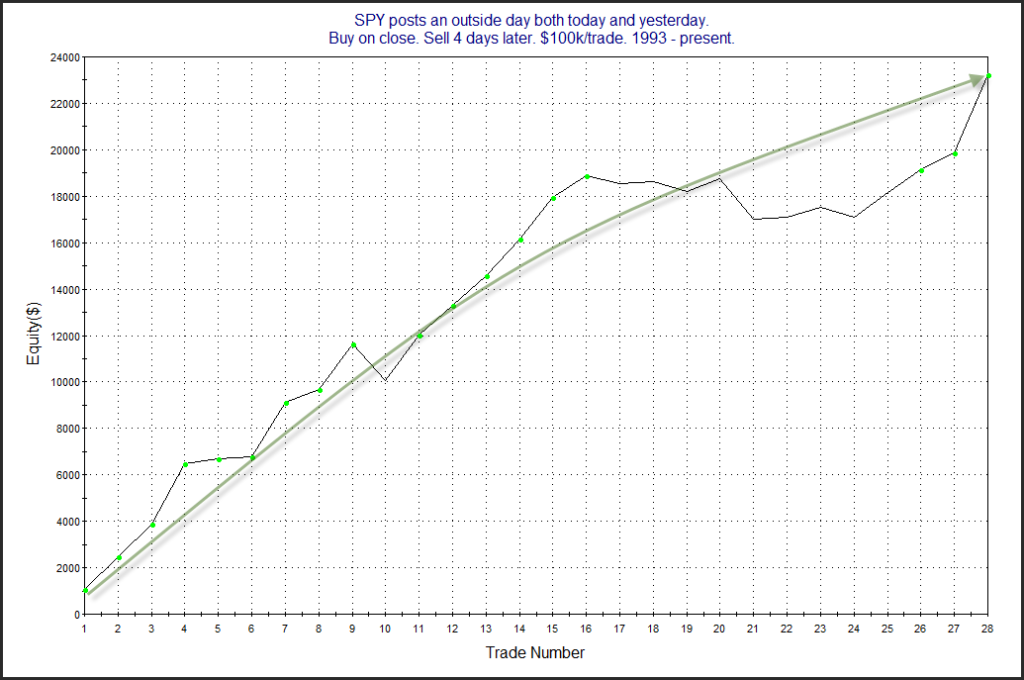

Notable about Tuesday’s action is that it marked the 2nd day in a row that SPY posted an outside day. (An outside day is a day where the security or index makes a higher high and a lower low than the day before.) I last discussed back-to-back outside days in the 7/28/16 letter. I have updated those results below.

The numbers look very impressive. Most of the upside edge has been realized in the 1st 4 days. Below is a profit curve using a 4-day holding period.

The move up is impressive and encouraging for the bullish case.

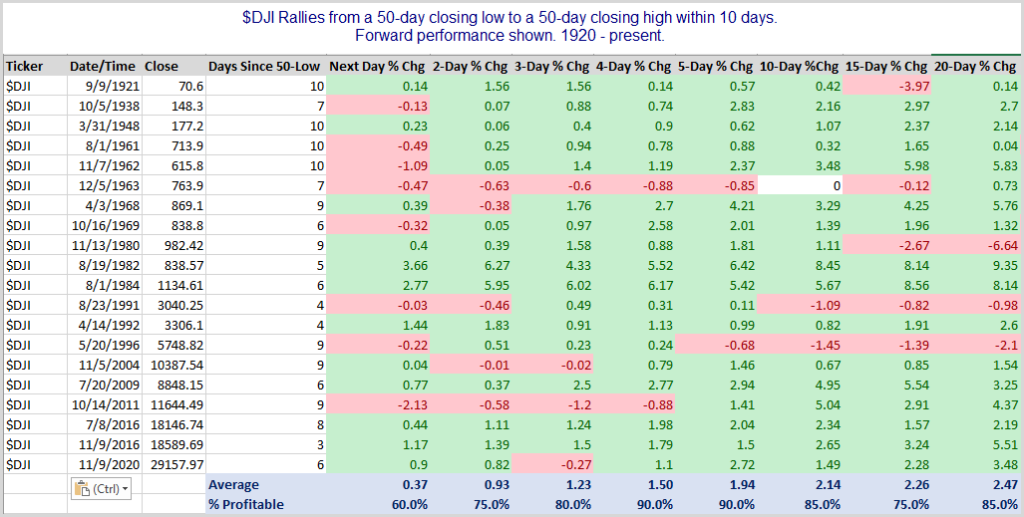

The SPX, Dow, and NASDQ all closed at all-time highs on Friday. Just 10 days ago the Dow closed at a 50-day low. That quick of a move from low to high is quite an accomplishment. Over the last 101 years this just the 21st time the Dow has managed to move from a 50-day closing low to a 50-day closing high within 10 days. Below are all the other instances, along with the $DJI performance in the following days and weeks.

The Dow has generally seen the upward momentum continue. Those are some impressive gains over the first 1-5 days, and even out through 20 days. Traders may want to keep this in mind when formulating their bias.

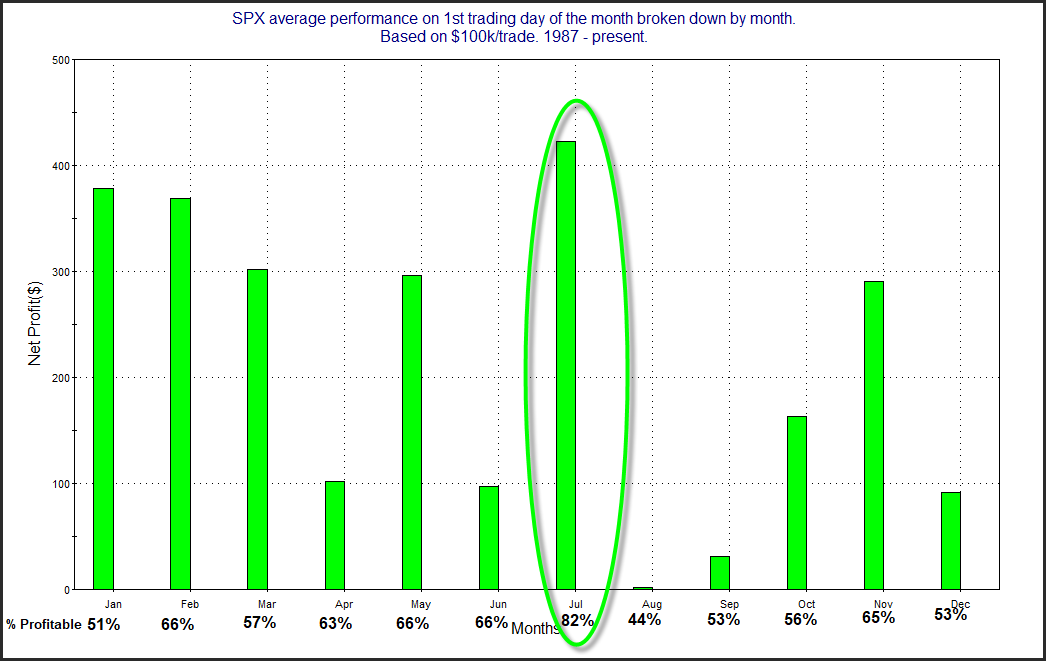

Since the late 80s there has been a tendency for the market to rally on the first day of the month. One theory on why this occurs is that there are often 401k inflows that are put to work on the 1st of the month. I examined this tendency and broke it down by month here on the blog a few times over the years. I decided to update the study again today.

The only month that comes even close to July from a Win % and Avg Trade standpoint is February. I’ll also note that August is the worst performer of any month.

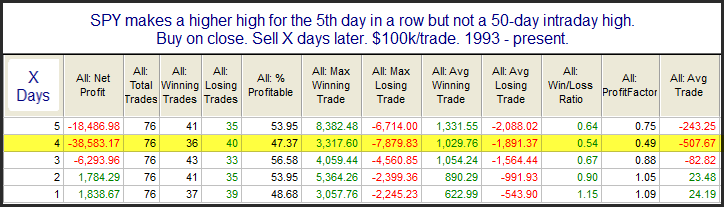

SPX managed to make an intraday high for the 5th day in a row on Friday. An interesting study from the Quantifinder looked at the possible impact of 5 higher highs occurring. The studies examined the impact of the position of the market when the 5 higher highs occurred. I broke it down again over the weekend. I wanted to see all times the 5 higher highs were accompanied by a 50-day high versus times they weren’t. First let’s look at times where 5 higher highs occur without a 50-day high.

Stats over the 1st few days suggest a possible mild downside edge. After 5 higher highs the market will sometimes need a breather.

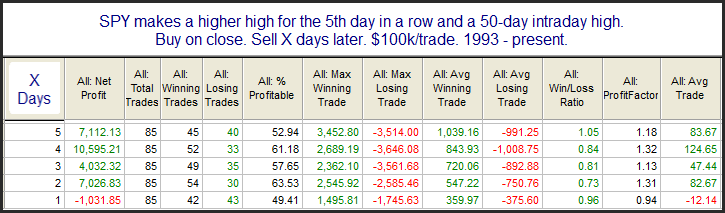

But what of times (like now) when a strong uptrend exists, and the market is also making a 50-day high? Those stats can be found below.

Interestingly, the number of instances has been nearly the same. But with an intermediate-term rally also occurring the tendency to pull back no longer exists. So the 5 higher highs are really of no concern in situations like the current one.

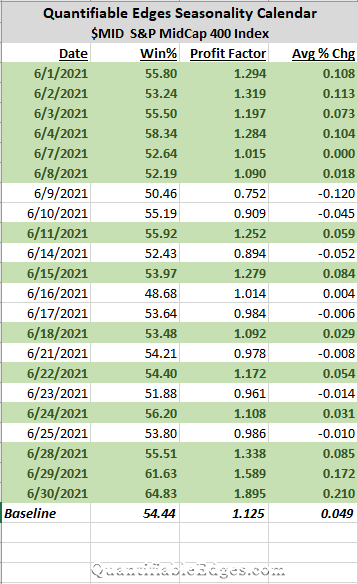

I have begun sharing one of the Quantifiable Edges Seasonality Calendars each month. This month I decided to show the S&P Midcap 400.

The Quantifiable Edges Seasonality Calendar uses multiple systems to measure historical performance on similar days to those on the upcoming calendar. The systems look at filters like time of week, month, year and so forth. Over the long run, staying out of the market on days that do not appear in green, would have been beneficial. To appear in green the date needs to show a historical Win% of 50% or more and a profit factor of 1.0 or more.

We see some solid seasonal numbers to start off the month. Then it is a mixed bunch for a few weeks. The strongest numbers in June appear in the last 2-3 days. Of course there will be many other factors impacting market action. But historically, avoiding days that do not appear in green has proven beneficial across all the markets we track. This is discussed in the “50/1 Calendar Research Paper”, which is available on the Seasonality page in the client section of Quantifiable Edges. It is available to all subscribers, including those on a free trial.

In the 4/12/19 blog I showed a study about US tax day (normally April 15th). The reason tax day may be important is that it is the last day that people can make IRA contributions to count for the previous tax year. This can create a last-minute rush and you will often have an inflow of funds heading into the market right around and on the day taxes are due. Fund managers will often put this money to work immediately and it creates a positive bias for the market. Below I have updated the study.

Futures are struggling in the overnight. Let’s see if this seasonal tendency can turn it around by the close today.

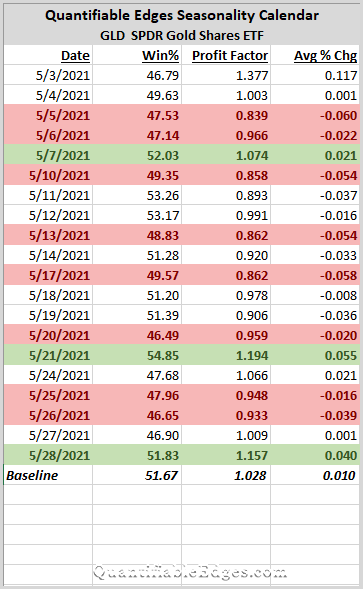

I have begun sharing one of the Quantifiable Edges Seasonality Calendars each month. Last month, we looked at the NASDAQ. This month the calendar that caught my eye was GLD, the Gold ETF. It looks lousy (technical term term for “sucky”).

The Quantifiable Edges Seasonality Calendar uses multiple systems to measure historical performance on similar days to those on the upcoming calendar. The systems look at filters like time of week, month, year and so forth. Over the long run, staying out of the market on days that do not appear in green, would have been beneficial. To appear in green the date needs to show a historical Win% of 50% or more and a profit factor of 1.0 or more.

Obviously, what stood out with regards to GLD is how bearish it appears. Only 3 “green” days all month is the worst for any of the 10 indices/securities we publish. The Baseline hurdles are fairly low, and they are rarely exceeded in the May calendar. Seasonality is just one factor, but I have found paying attention to it to be worthwhile. A couple of months ago, I published a research paper that showed the value of avoiding gold on days that did not show favorable seasonality odds. That paper is available to all subscribers, including trial subscribers, on the Quantifiable Edges Seasonality page. It is titled “Gold 50/1 Calendar Model Research”.