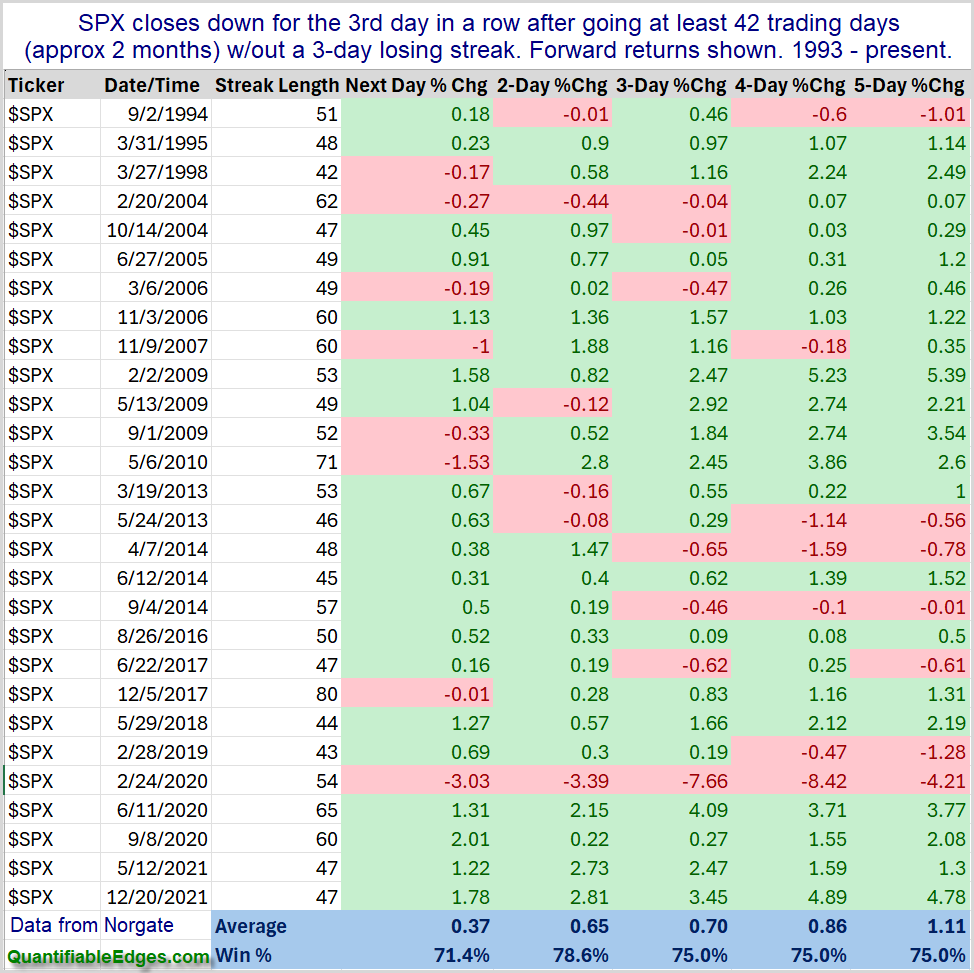

Friday on X (Twitter) I noted that the 3-day pullback for SPX would be the 1st one since early January. SPX had gone 48 days since the last time it had a 3-day pullback. I looked back at other times SPX went at least 2 months without a 3-day pullback, and examined performance after it finally arrived. This can be seen in the table below.

Results over the next 1-5 days are compelling, and suggest a strong bullish tendency. Traders may want to keep this in mind when setting their short-term market bias.

I was honored to be interviewed by Brian McAboy last week on the Consistent Profits Podcast. You can find it using the link below. It is also available on all the typical podcast platforms.

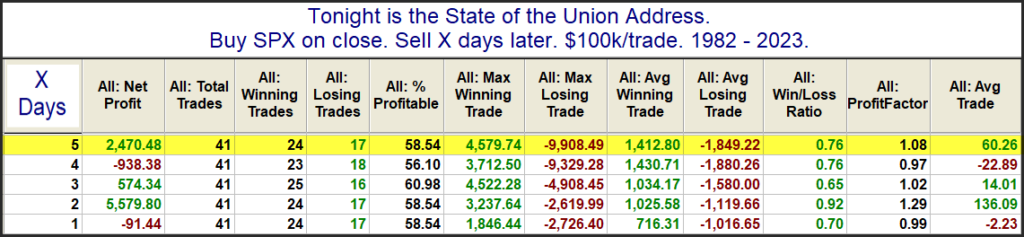

Joe Biden will be giving his State of the Union Address tonight, and people are wondering how his talk might impact the market over the next several days. I have looked at performance following State of the Union before and decided to update that research today. The data table below looks back to 1982. There were a few instances, such as 2001 and 2009 where the speech was not an official “State of the Union”, but was delivered under a different name. I have included those speeches in the results as well.

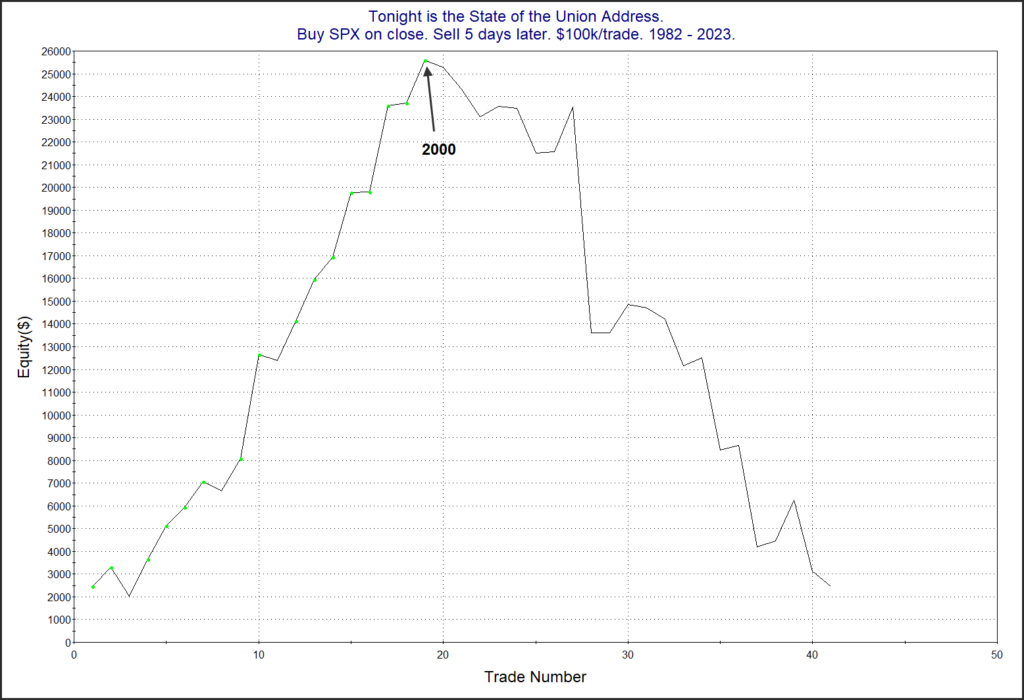

The stats do not suggest much of an edge. But the profit curves seem to tell a more interesting story. Here is the 5-day curve.

All the curves look something like this in that since the turn of the century (Bill Clinton’s last year) the market has tumbled after these speeches rather than been inspired by them. I guess they just don’t give speeches like they used to.

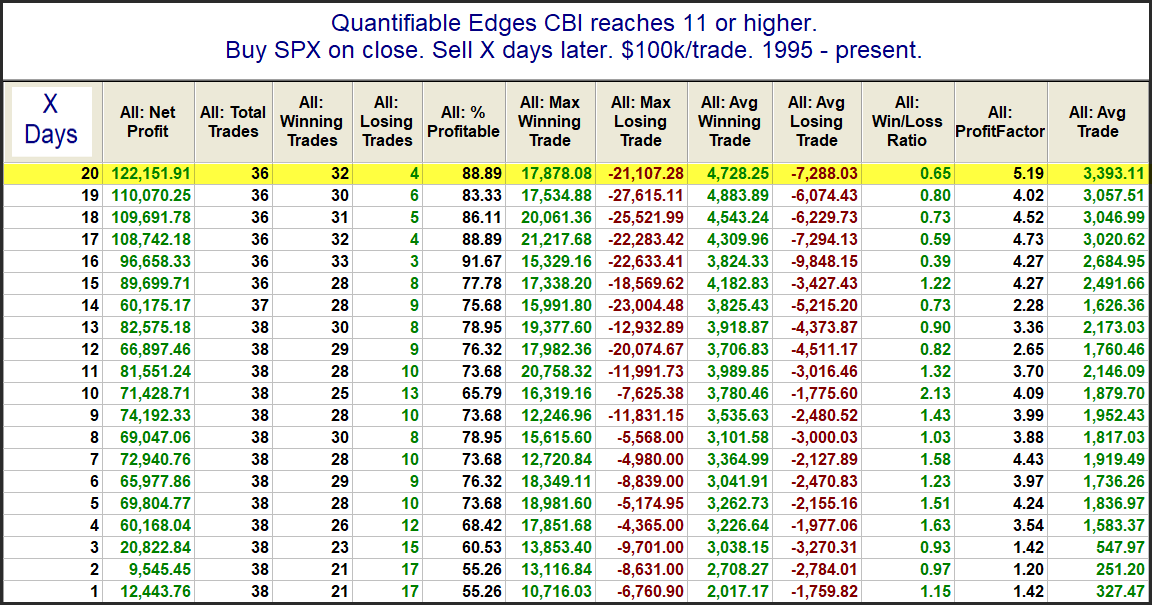

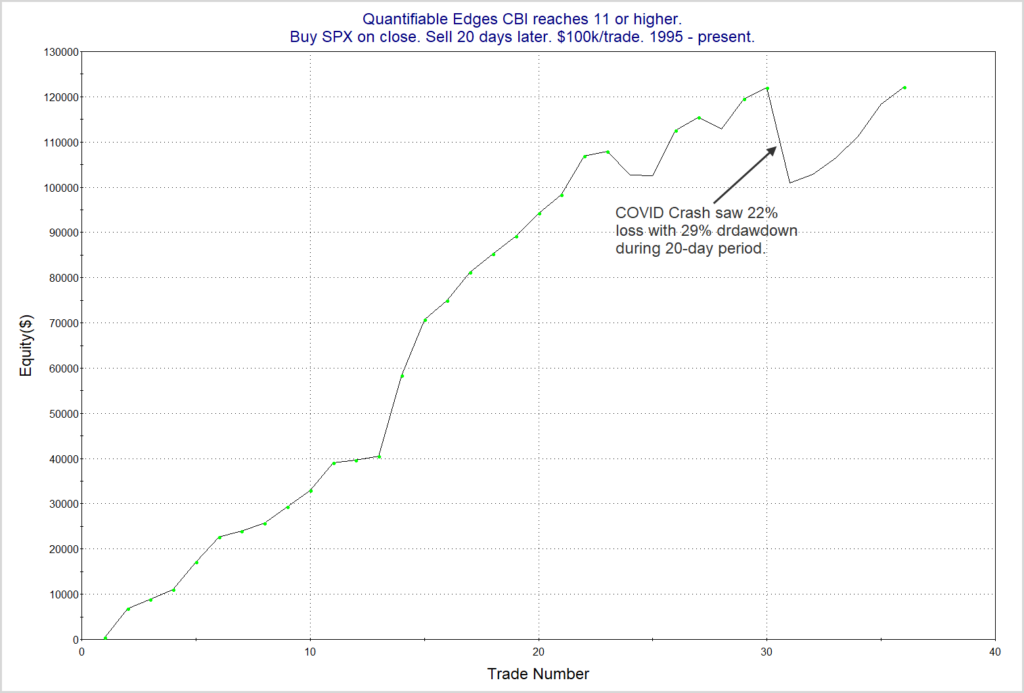

Especially notable about Friday’s action was that the Quantifiable Edges Capitulative Breadth Indicator (CBI) rose to 11. This is the highest level it has been at since September of 2022. Below is a quick look at CBI readings over the last 2 years. I have shown dotted lines each time that it reached as high as 9.

I have generally viewed 10+ as strongly bullish over the years. I have also shown in the past that readings of 11 or higher have been a bullish intermediate-term indication. This can be seen in the study below.

Looking out over the next several weeks, the stats are (almost) all very impressive. The one exception is the Max Losing Trade. That was thanks to the COVID Crash in March of 2020. Below is a profit curve using the 20-day exit strategy.

Even with the COVID Crash included, this study has made it back to new highs. Overall, I view the CBI spike over the last few days to be a favorable indication for both the short and intermediate-term.

QQQ, on a dividend-adjust basis, is now up over 52% on the year and just made new highs. This can be seen in the monthly chart below.

Meanwhile, TQQQ, which is the 3x version of QQQ, is up over 185% ytd (through 12/13/23). That’s a huge run, and on the surface it would seem to be an enticing long-term holding. But here is the TQQQ chart.

As you can see, TQQQ is still nearly 46% below its all-time (dividend-adjusted) high of $90.08. To get back to a new high, it is going to need to make another 85%. That is some severe underperformance vs QQQ over the last 2 years.

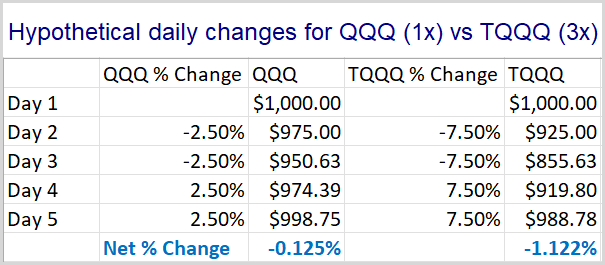

So what gives? It is mostly just a math issue. Leveraged ETFs like TQQQ utilize leverage on a daily basis. TQQQ is a 3x leveraged ETF. So a 2.5% up day for QQQ would be about a 7.5% up day for TQQQ. And a 2.5% down day for QQQ would be about a 7.5% down day for TQQQ. When the market gets volatile and choppy the swings back and forth will hurt TQQQ more than QQQ.

Let’s look at a simple example. QQQ goes down 2.5% for 2 days in a row, and then bounces back 2.5% for 2 days in a row. These are fairly large 1-day moves, but it demonstrates the point nicely. Below is a table showing daily changes for each and the value of the holding over the period.

Keep in mind that smaller drawdowns are easier to overcome than large ones. A 10% drawdown would bring an account from $1000 to $900. To get back from $900 to $1000, you would need to make $100 from the account that is now only worth $900. This would require an 11.1% gain on the $900. As the drawdowns get larger, you end up needing much larger % gains just to recover to the original $1000. A 50% drawdown would take a $1000 account down to $500. To get back to $1000, that account would now need to make 100%! A 90% drawdown would turn a $1000 account into a $100 account. To get back to $1000, you’d need to make 900%!!

So in the table above we see that QQQ has a drawdown that is substantially less extreme than TQQQ. Therefore, it requires much less work to get back near breakeven. At the end of the 4-day move, QQQ is down just 0.125%. But TQQQ is down nearly 1% more than that, with a 1.122% decline. And these are not huge moves, and it is not a long period of time. Larger moves and longer time periods really exacerbate the situation.

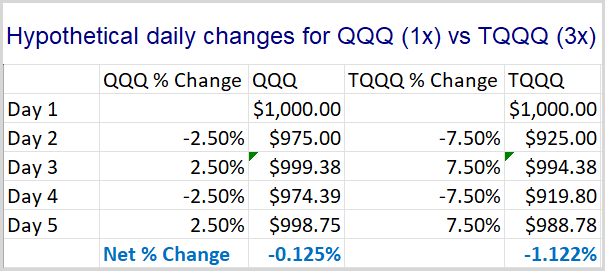

Now you may be thinking, “Yeah, but you put the two worst days first. That makes it even harder to recover. So the difference is exaggerated.” No – it isn’t. In fact, it does not matter at all what order I put the days in. The results will be the same. The spreadsheet below shows the same daily returns, except in this case, they alternate down-up-down-up.

The end result is exactly the same. You can run it in different orders yourself if you don’t believe me. The end result will remain the same. And the bigger the daily moves, the more negative the impact.

So when QQQ suffered a 37% drawdown from it November 2021 high, TQQQ was hit with a drawdown of over 82%. To get back to even from there, TQQQ would need to make back over 450%! And as we saw in the chart above, it is not even close.

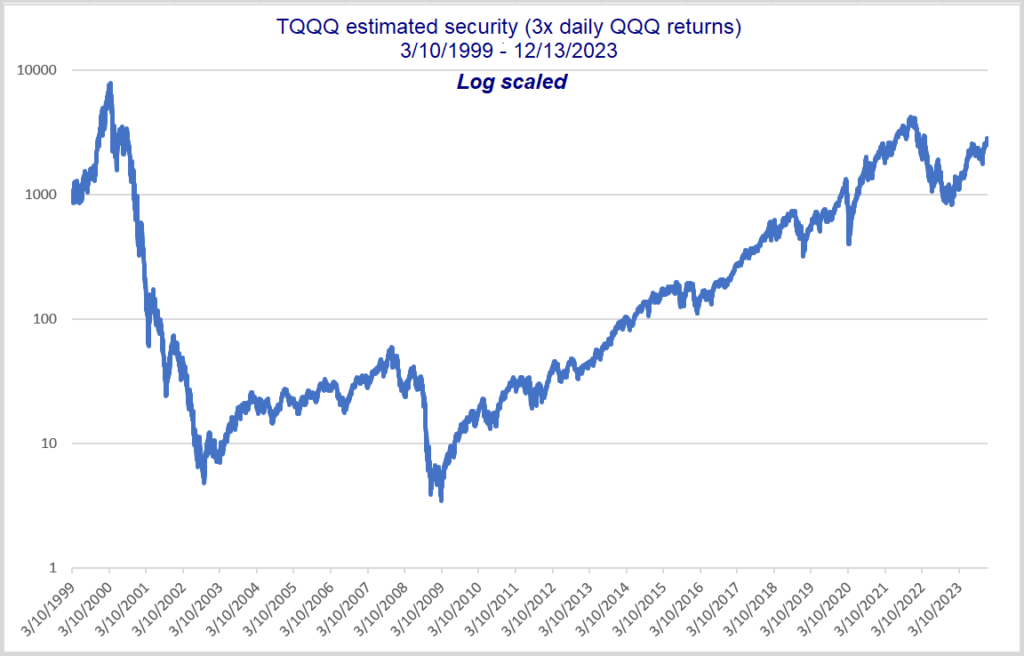

You might not yet be convinced of the danger of TQQQ. After all, that long-term chart is still showing massive gains over the last 13 years or so. In fact, TQQQ opened on 2/11/2010 with a dividend and split adjusted price of $0.423931. It currently has return of 11,397% since inception. That blows away the 951% return of QQQ over the same period.

But perhaps TQQQ’s inception date was just exceptionally good timing. What would happen if TQQQ started on the same day as QQQ?

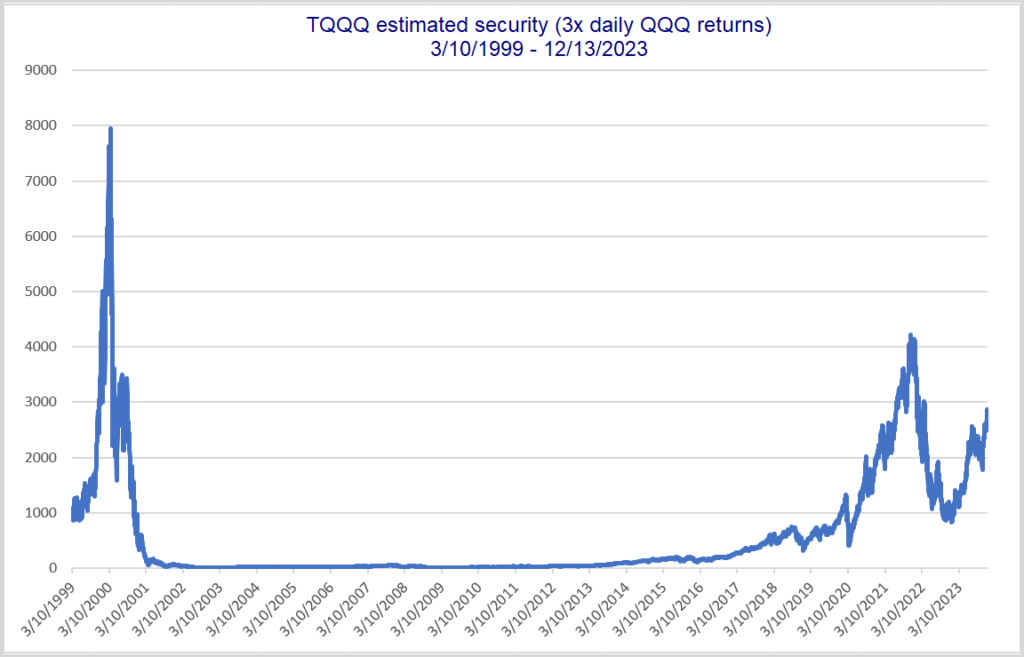

To answer this I created a TQQQ substitute security (TQQQx) with data going back to QQQ inception (3/10/99). I did 3x returns each day. Below is a hypothetical price chart for TQQQx:

Current price of $2862 means it is still in a 64% drawdown. This estimated TQQQ would need to see a rally of 178% to get back to its high from 2000. Here is a log scale version.

You can see here more easily that the price went from a high of $7961 to a low of $3.47, which is a 99.96% decline. Anyone holding would basically have been completely wiped out – especially if they needed to make withdrawals.

Lastly, I will note that my calculation is overly generous because there are no management fees. If I plug in the split-adjusted TQQQ price of $0.423931 as the 2/11/2010 price in my spreadsheet, it shows a current value of $81.40, instead of the actual TQQQ price of $48.74. In other words, my numbers are too optimistic, and the reality would have been even worse than I show.

Working at CA360, I have encountered multiple people that made a fortune over the last 10-13 years by simply holding onto a sizable TQQQ position. But as we see above, leverage can make fortunes, and it can also destroy them. The 2000-2009 decade provides a great example of destruction. Leveraged ETFs should be used with great caution. There’s no telling what the next 10 years will look like. But there is a strong chance it won’t be as friendly as the last. If you utilize leveraged ETFs, an exit plan needs to exist. You don’t want to ride out an 82% drawdown at any age…and you especially don’t want a 99.6% drawdown! Buy(and hold)er beware.

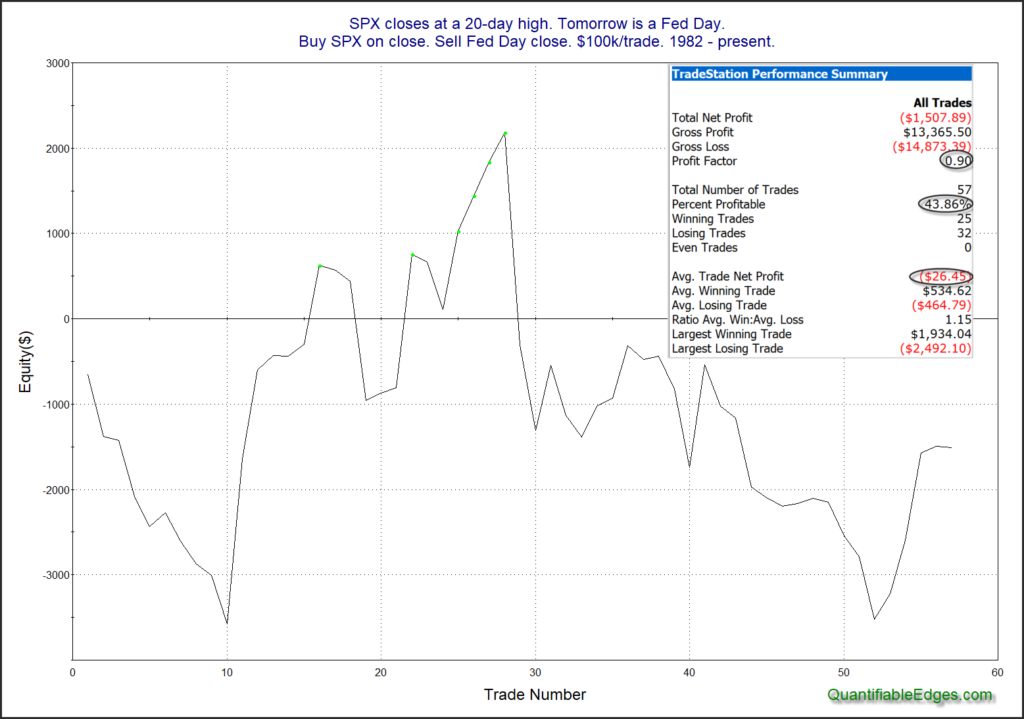

Wednesday is a Fed Day. Fed Days have historically shown an upside tendency. I have documented this tendency in great detail over the years. A higher close today would not be the most favorable Fed Day setup. A big reason for this is that it would mark a 20-day high close. Fed Day bullishness has often occurred when a Fed announcement has helped to alleviate market stress. When the market closes at a 20-day high, it typically means there isn’t a lot of worry present. Under these circumstances, the upside inclination has also not been present. This can be seen in the study below.

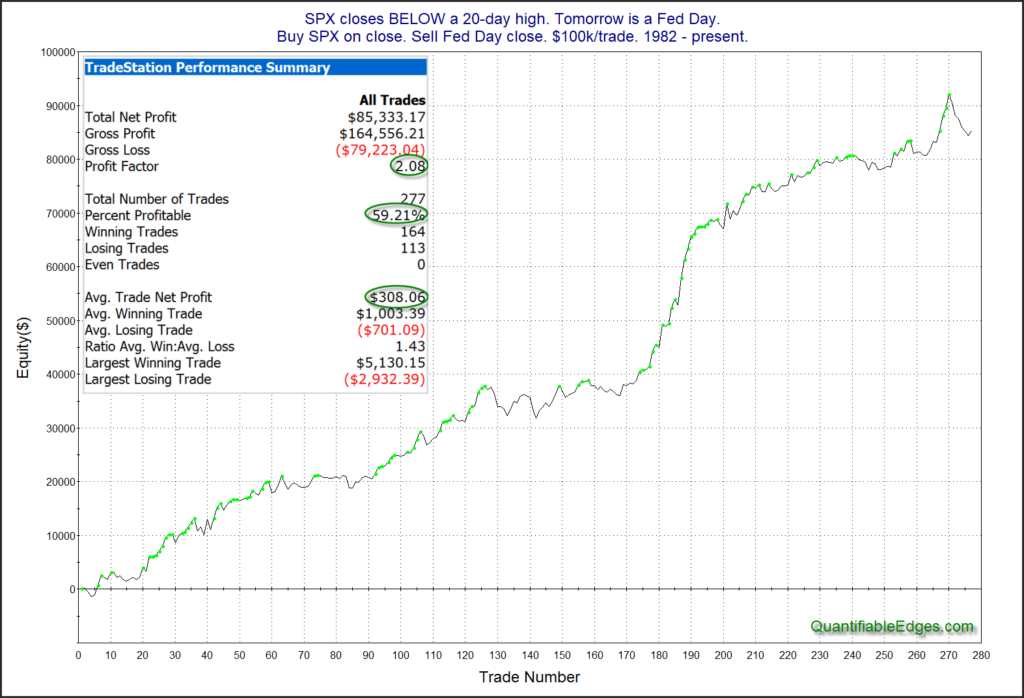

Neither the stats table nor the profit curve suggest any consistency or tradable edge. As a comparison, here is a profit curve of all Fed Days when SPX did NOT close at a 20-day high the day before.

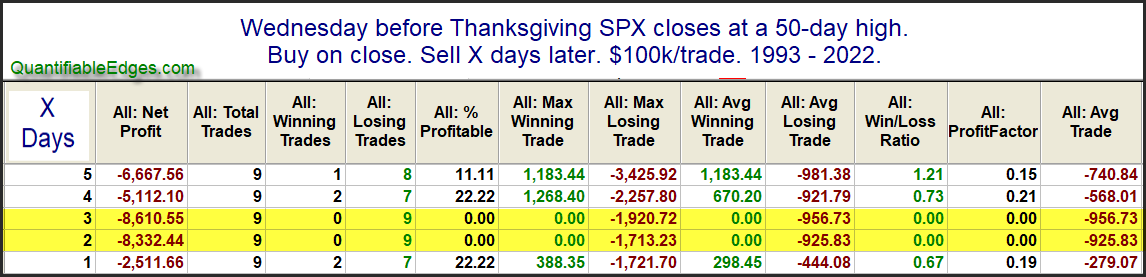

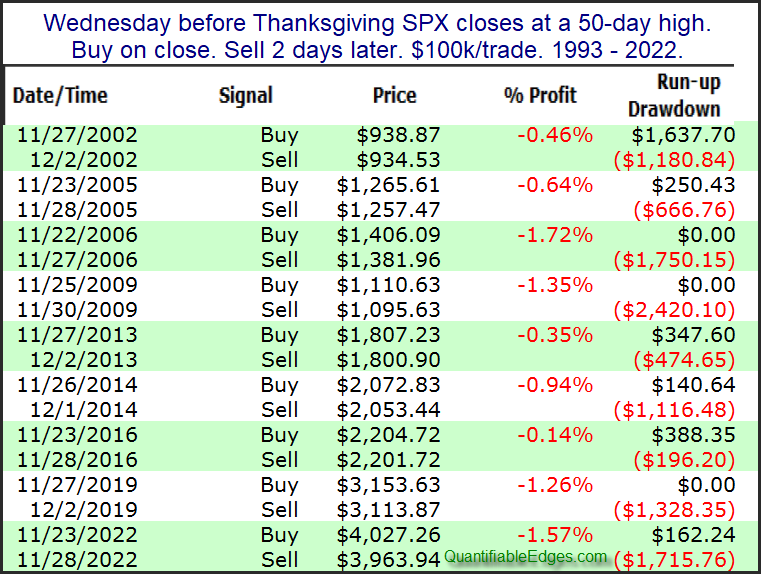

This year we have seen strong upward momentum heading into Thanksgiving, with SPX closing at a new intermediate-term high on Wednesday. I decided to look back at other times SPX closed at a 50-day high on the day before Thanksgiving.

Results over the next 1-3 days appear quite bearish. I will note that there were a couple instances that occurred just prior to the sample set that were mildly positive over the 2-day period. But the poor performance over the last 30 years (9 instances) is notable and interesting. Below is the list of instances.

Traders may want to take this under consideration when setting their trading bias over the next couple of days.

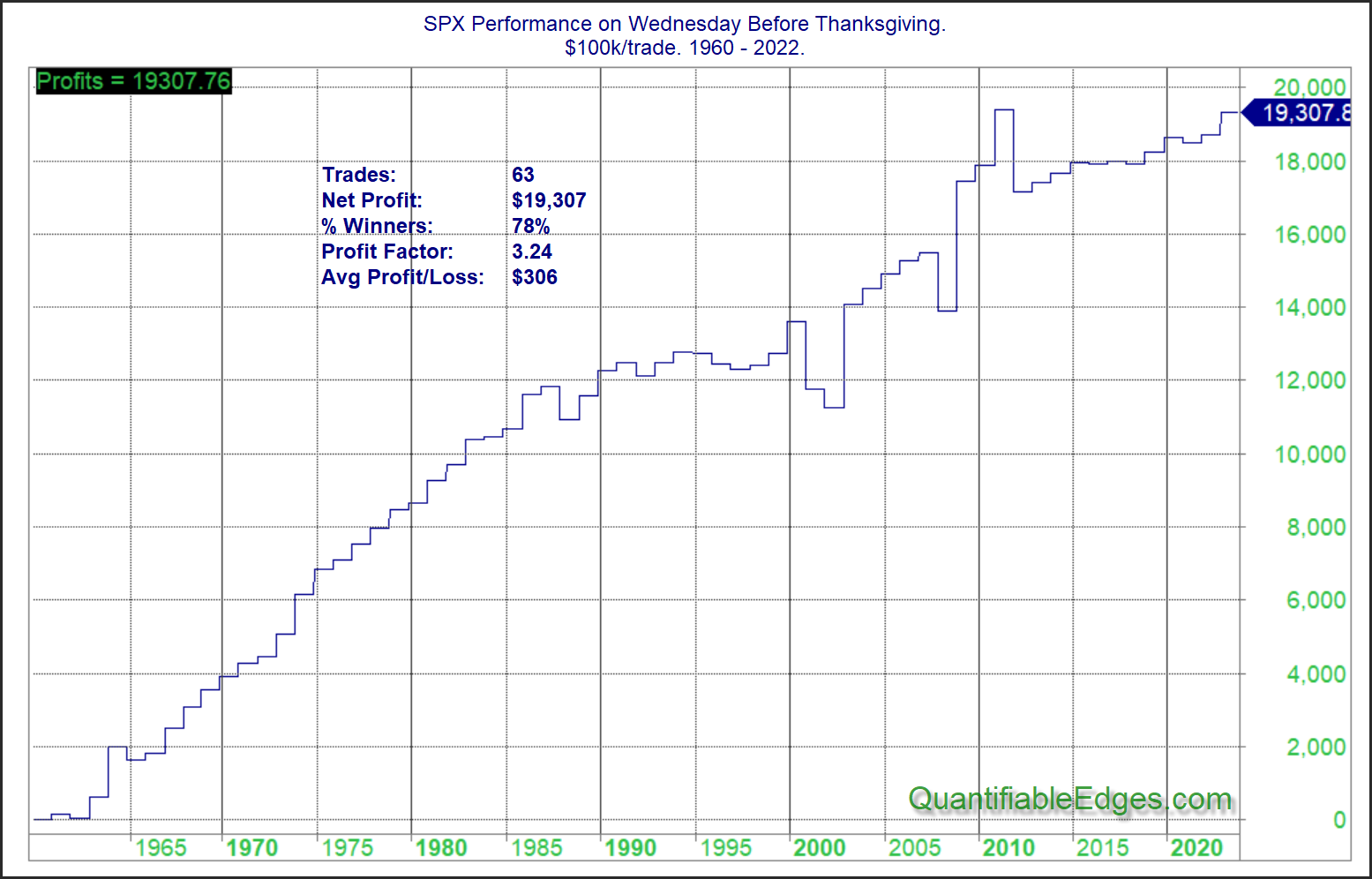

Thanksgiving week has shown some strong seasonal tendencies over the years. I’ve documented this in years past on the blog. From a seasonal standpoint, Wednesday before Thanksgiving is one of the most bullish trading days of the year. The chart below shows performance from Tuesday’s close to Wednesday’s close on the day before Thanksgiving.

It certainly appears seasonality will be providing a wind at the market’s back on Wednesday. Happy Thanksgiving!

On Thursday November 16th (and again on Monday) I will provide followers with a webinar on “Enhanced Portfolio Construction”. I will be discussing usage of diversification, leverage, and margin, and how I incorporate them into portfolios for my clients.

On Thursday 11/16 at 1pm EST, and then again Monday the 20th at noon I will be hosting this special free webinar. Details can be found below.

Date and time: 11/16/23 at 1pm (Eastern Time) & again 11/20/2023 – noon (Eastern Time)

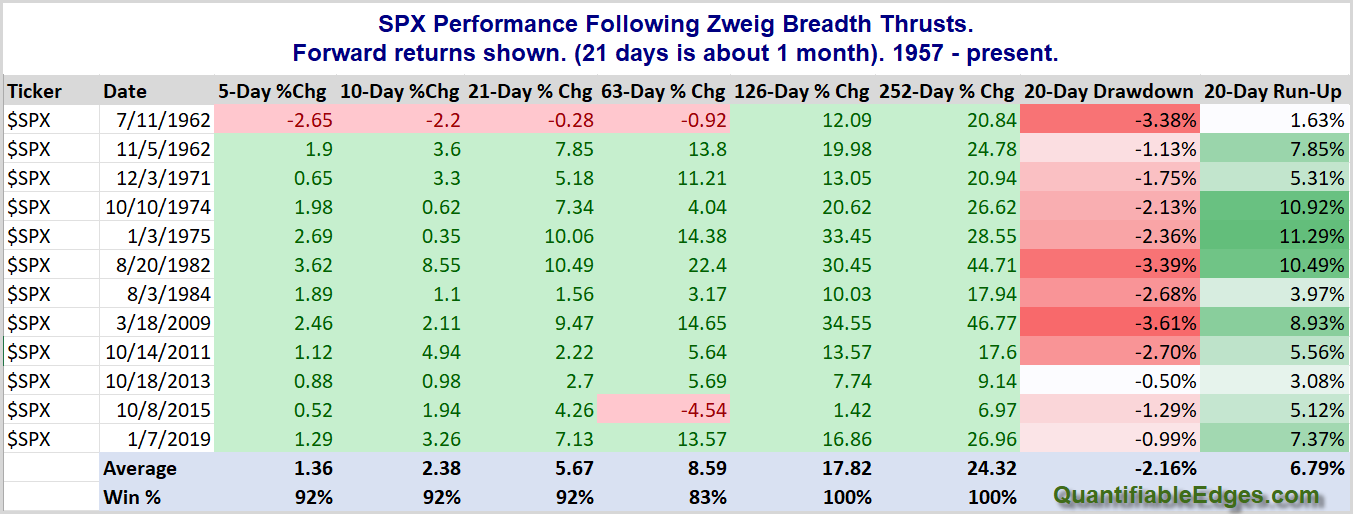

The strong breadth we have seen recently has caused the 10-day exponential moving average of the Up Issues % to rise up to 63.6%. A move through 61.5% after being below 40% within the last 10trading days is considered a Zweig Breadth Thrust trigger. This is a signal created by Martin Zweig. I last discussed it in the 1/8/19 blog. In that post I also showed charts for past signals. Over the long haul Zweig Breadth Thrusts have been rare but powerful. Below is a stats table showing results of all signals since 1957 and summarizing them. (Note I used Norgate Data this time, rather than Tradestation data. That was so I could look back further in time. Data providers data often varies slightly, so we see a 2011 instance below where we did not see that with the Tradestation data a few years back.)

Over the short, intermediate, and long-term there have been strong gains on a consistent basis. The AVG run-up over the next 20 days has been 6.79%. This is double the MAX drawdown, and over triple the average drawdown. Average gains over the next 10 days are 2.4%, 21-days average 5.7%, and the average gain over the next year has been 24.3%. Those are impressive moves. So yes, the market is overbought. But this is a case where the move has been so strong and so broad that strength is likely to beget more strength.

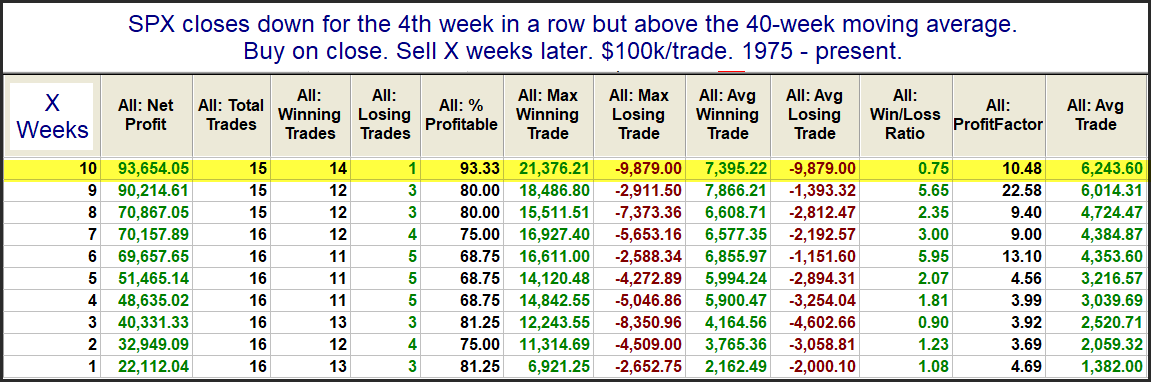

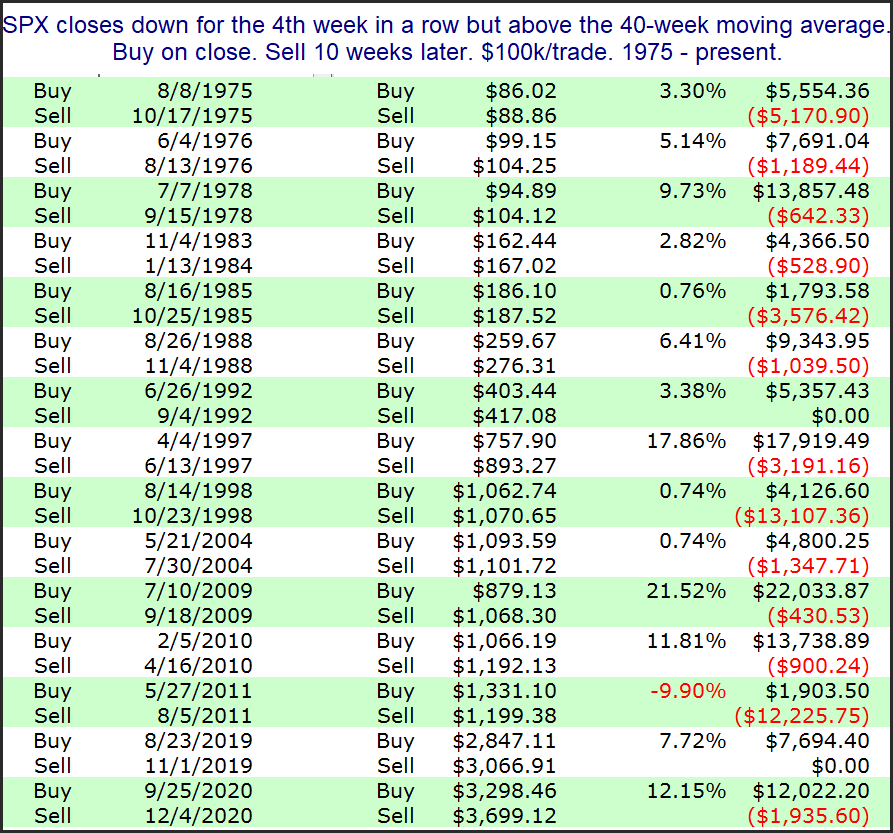

This past week was the 4th week in a row that the SPX declined. It is quite unusual to see SPX close down for 4 weeks in a row, but still remain above its 40-week moving average. Below is a look at other times since 1975 that this action has occurred.

These results are suggestive of an upside edge over the next several weeks. Below I have listed all 15 non-overlapping instances using a 10-week exit strategy.

The 2011 instance did not work out at all. Most everything else looks encouraging. Based on this narrow look, it appears we are reaching a point where an SPX rally might be expected in the coming weeks.

One particularly notable indicator change that occurred at the close on Friday is that out NASDAQ/SPX Relative Leadership indicator flipped so that it is now showing the SPX as leading and the NASDAQ as lagging. This can be seen in the chart below.

Whenever the solid (green/red) line is above the blue dashed line that means the NASDAQ is leading. When it drops below (and turns red as it is about to do), that means the NASDAQ is lagging the SPX. The market has performed substantially better over the years when the NASDAQ has been leading. You can see in the chart above that the NASDAQ has been the leader for most of 2023. SPX was the leader for most of 2022 as the market struggled overall.

This could be a brief headfake like we saw in April. But it is certainly notable that NASDAQ is no longer the stronger of the two indices. And that is generally an unfavorable condition for as long as it persists.

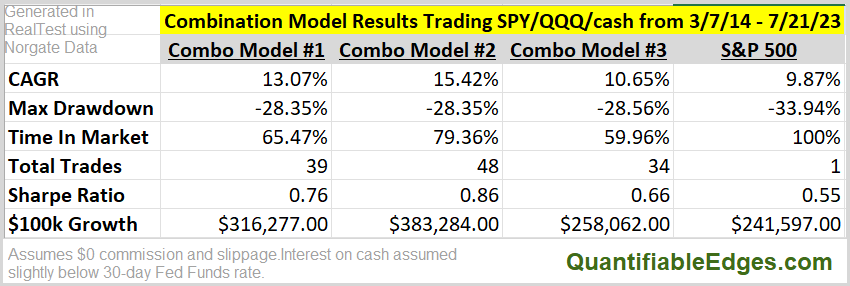

Quantifiable Edges Market Timing Course was originally released in 2014. Since then, the Combination Models presented have all soundly outperformed the S&P 500 (as shown in the table below).

Quantifiable Edges just released its 2nd edition of the course, with updated stats for the 4 original indicators and 3 original combo models. But we are also expanding the course to include a new Fed Liquidity indicator and new combination models to incorporate this new, powerful indicator.

The table below shows performance of the 3 original combination models since the release of the Quantifiable Edges Market Timing Course over 9 years ago.

All 3 models have achieved higher returns with less drawdown and reduced market exposure in live action over the last 9+ years!

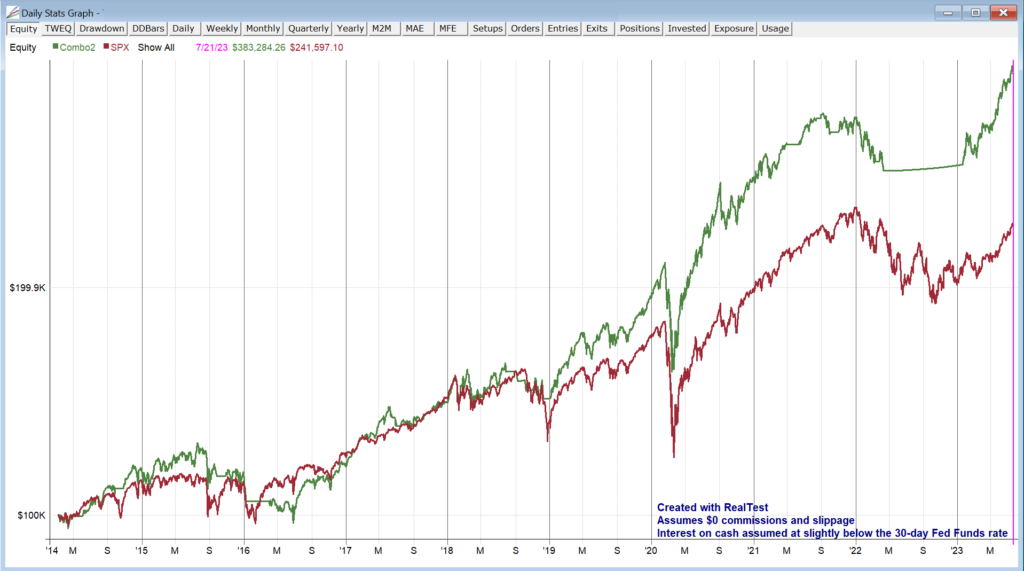

Combination #2 is the most active and aggressive version. It has been in the market about 79% of the time since it was 1st published. Over that time, there have only been 48 trades (about 5 per year), and it generated a compound annual return that outpaced the S&P 500 by 5.55% per year! Below is a profit curve of the model vs the S&P 500.

The chart was created using RealTest software, and RealTest users can easily reproduce it with the add-on code.

Now with the updated and expanded 2nd edition of the course, Quantifiable Edges introduces its Fed Liquidity indicator. The indicator is grounded in Fed-based work that Quantifiable Edges has produced since 2012. And as you’ll see in the analysis, the Fed Liquidity indicator would have acted as a better predictor of SPX movement over the last 20+ years than any of our original 4 indicators.

We then share some ideas and sample models showing how incorporating the Fed Liquidity indicator along with the original models would have produced even more impressive results than the original Combo Models.

Also covered in the course are ideas for execution, potential improvement on the models, and how they could be incorporated into someone’s portfolio.

The indicators and models are all fully open.

Excel, Tradestation, and Ninja-Trader code is available for free for the original 4 indicators.

RealTest and Amibroker code is available as an add-on.These allow you to reproduce the results of the Combination Models, tweak them however you please, and explore the indicators and ideas further!

Additionally the original course is still available for students to view and refer to so that they can easily see what was taught 9 years ago, and how it has held up over time!

Anyone can build a nice-looking backtest. Live performance is what matters. The Quantifiable Edges Market Timing Course has delivered since it was released in 2014. So sign up today, and gain a quantifiable edge over most investors! (Or sign up for an annual Gold or annual Silver subscription and get the 2nd edition of the Market Timing Course for free!)

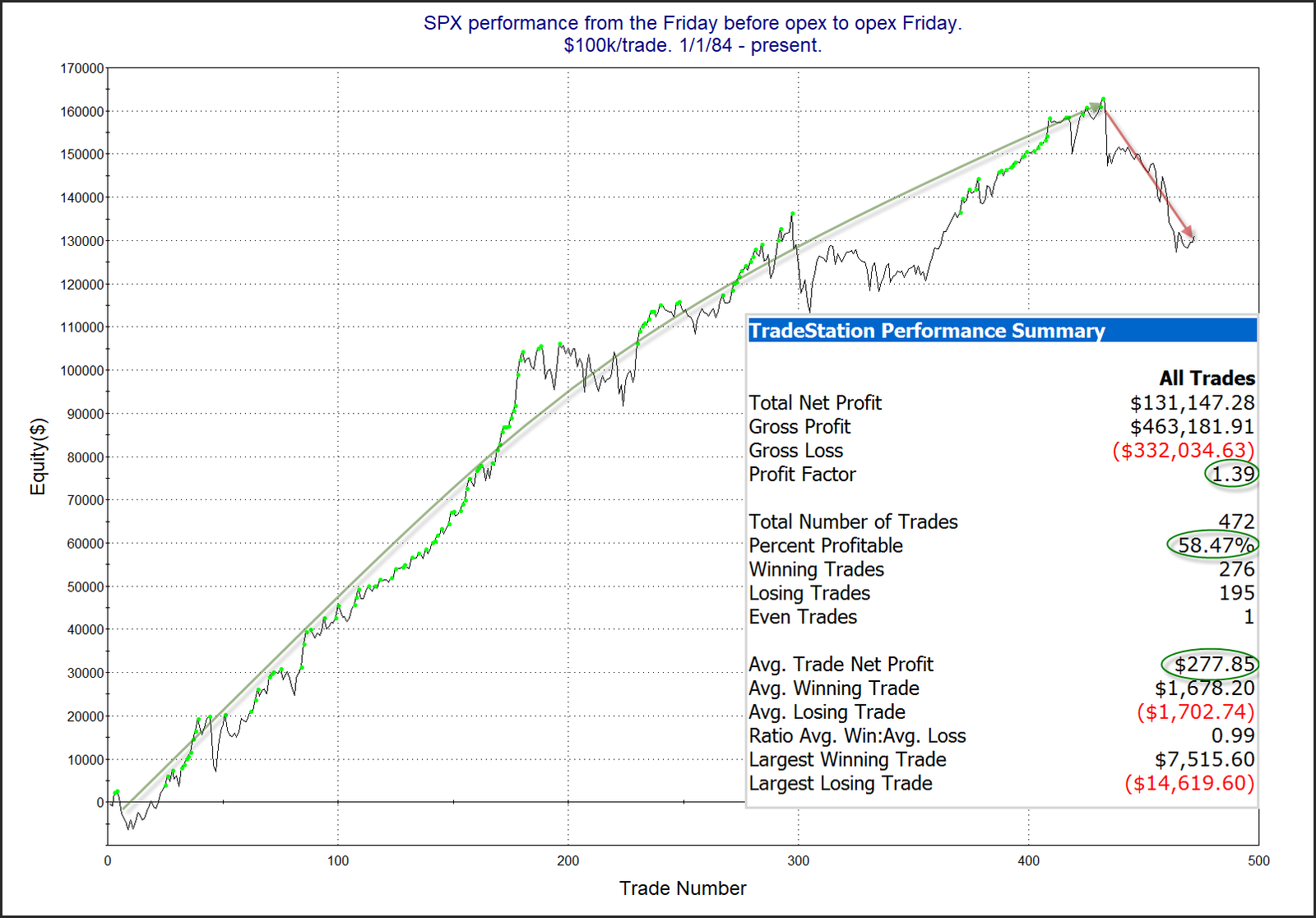

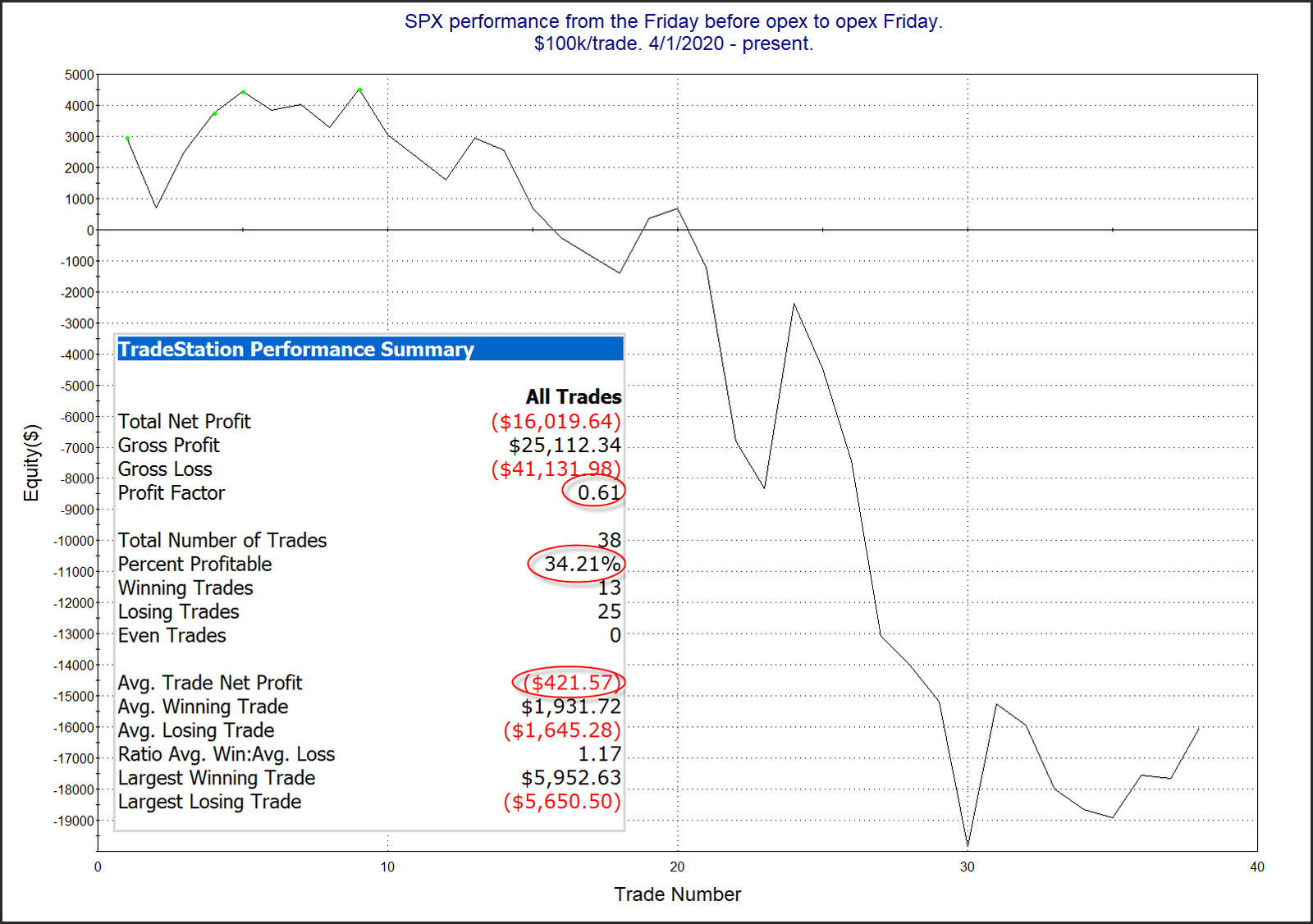

This week is options expiration week. And we have known for a long time that opex is often a bullish week for the market. Interestingly, that seasonal tendency has not seemed to hold true since the COVID crash in 2020. Below is a look at performance of all opex weeks since 1984.

There has been a clear shift in the curve over the last few years. The top of this curve came in January of 2020. February of 2020 saw a decline of 1.25%, and then March had the worst opex week ever, with a 14.6% drop. But unlike other periods, opex week has never recovered its bullish tendency. The chart below looks at performance since April of 2020. I started the chart at that point simply to see how it has done since the market bottomed in 2020. So this does NOT include the worst week of March 2020.

There has been a little bit of a bump up over the last few instances, but the stats and curve still look pretty awful. I am not yet convinced that downside tendency of the last few years is a new seasonal trend. But I certainly see enough evidence here that I am no longer looking at opex weeks and automatically thinking they are bullish.

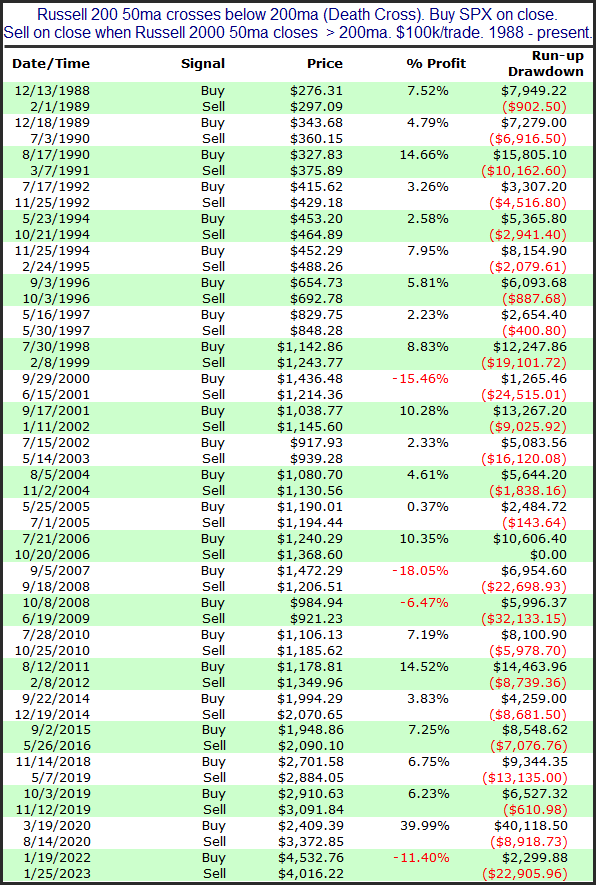

I have seen some chat about the Russell “Death Cross” that occurred on Friday and the potential bearish implications for the market. A “Death Cross” is a catchy (though not terribly accurate) term for when the 50-day moving average of a security cross below its 200-day moving average. It is sometimes promoted as a warning of a potential bear market. Of course all bear markets will see this happen at some point, because a bear market is an extended decline. But the real question when considering the implications of the Death Cross are whether it serves any value in predicting a more substantial decline. A few years ago I did an examination of past Russell Death Crosses, and what they meant for the S&P 500. I have updated that study from the 11/14/18 blog below.

Both of my data sources show Russell data back to late 1987. And since I need 200 days to calculate a 200-day moving average, the earliest the study could look back to was 1988.

Here is the list of all Russell Death Crosses and how the SPX performed from the time of the initial cross until the Russell Death Cross was no longer in effect (meaning the 50-day moving average closed back above the 200-day moving average).

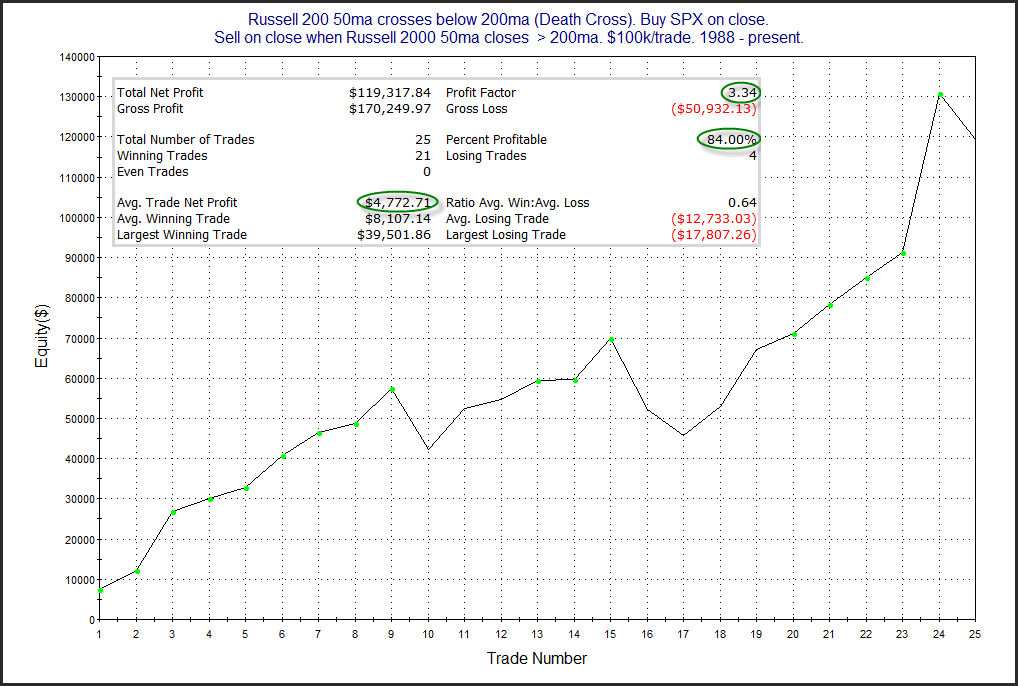

Twenty-one winners. Only four losers. So 84% of the “predictions” were wrong. The biggest winner of the group came in 2020. The most recent instance, from last year, saw a substantial loss. Here is a look at the summary stats and a profit curve for this setup.

I am having a hard time seeing the Russell 2000 Death Cross as a bearish indication. You would have a much easier time convincing me this is a bullish indication for the intermediate-term. (I don’t really view it as bullish though. Drawdowns were generally sizable, even for a good portion of the “winners”.)