This Strong Start Study Is Triggering Today

Strong move in the early going. According to my data, this old study has just triggered:

https://quantifiableedges.blogspot.com/2009/11/what-strong-early-tick-has-meant-in.html

Strong move in the early going. According to my data, this old study has just triggered:

https://quantifiableedges.blogspot.com/2009/11/what-strong-early-tick-has-meant-in.html

Monday’s bounce in reaction to Friday’s drop came on the lowest NYSE volume in a week. Below I have listed all instances since 2002 where the market has dropped 2% one day and then risen the next on the lowest volume in a week.

Studies were a bit mixed after Friday’s drop. There is certainly danger of more downside.

To understand why readers should reivew the study below from Feb, 2009.

https://quantifiableedges.blogspot.com/2009/02/importance-of-positioning-in-analysis.html

I’ve updated the Quantifiable Edges Big Time Swing System overview page with results through June 30. I don’t update it that often since the system only trades about once per month on average. I’m please to say that while the SPX was down 7.57% for the 1st half of the year, the QE Big Time Swing System managed to post a 0.93% gain.

This is well below long-term norms. So while it may seem a bit disappointing from that perspective, the fact that it has weathered such historically abnormal action the last six months is inspiring. January saw the market experience an abnormally sharp and persistent selloff. This was followed by one of the most persistent upmoves ever from Feb – April. We then had to deal with a one of a kind “flash crash” and then more extreme action culminating in a wicked selloff at the end of June that triggered numerous historical extremes.

With all that to think about, buy/sell decisions were easy for QE Big Time Swing traders. SPY had 7 trades trigger. Using the system, entries and exits are clearly defined and there are no extraneous variables to worry about. Of the 7 SPY trades, 4 were winners and 3 were losers for a net of 0.93% including commissions, dividends, and interest on cash (assumed at 0.16% annual this year). Again, not great, but not bad considering all the market dealt us the last 6 months.

Of course these results assume traders used SPY and took the “standard” entries and exits as published in the manual and sent to purchasers via email (free for 2010). One of the biggest advantages with the QE Big Time Swing System is that it is all open-coded and comes complete with a substantial amount of background historical research. Many system owners have either incorporated ideas for “tweaking” from the manual or used their own ideas to customize the system. Anyone doing this would have experienced different results.

For more information and to see the updated overview sheet, click here.

If you’d like additional information about the system, or have questions, you may email BigTimeSwing @ Quantifiable Edges.com (no spaces).

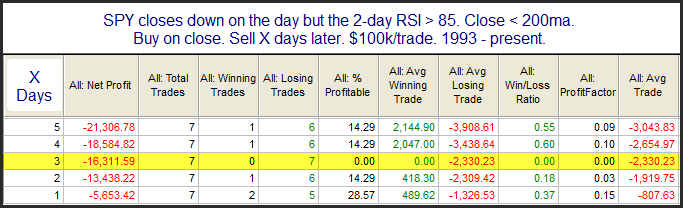

Below is one pattern I examined in last night’s Subscriber Letter that had interesting results.

To qualify for the study the market first needs to be very overbought and then second it needs to pull back extremely gently. The 2-day RSI is such a sensitive indicator that any decent pullback – even from a very overbought condition – would normally see it close below 85. While the sample size is very small, historically this has always been followed by a pullback.

Large gaps up like yesterday that reach new highs, go unfilled and finish above the open don’t often follow through over the short-term. Below is a study that appeared in last night’s Quantifinder that demonstrates this.

This study suggests a fairly potent downside edge over the next 3 days. Occurences are a little bit low but with only 25% of instances trading higher 3 days out and an average return of -1.4% I believe it is worth taking under consideration.

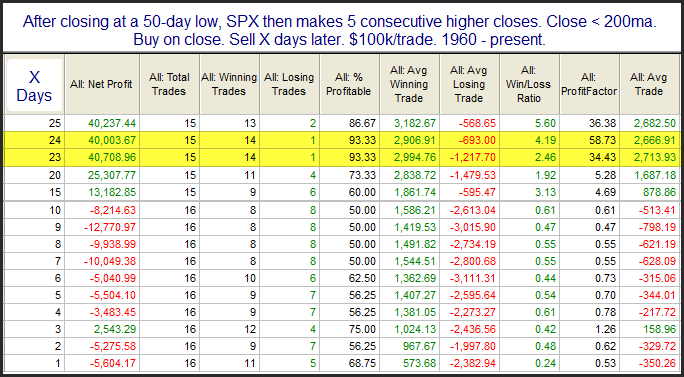

Monday marked the 5th higher close in a row. This kind of persistence coming off a low has almost always led to further upside over the intermediate-term. This can be seen in the study below.

Short-term returns were very choppy. Looking out a month or so the results strongly favor the bulls. In last night’s Subscriber Letter I listed all the instances. What was interesting is that there was positive representation from every decade.

It was pointed out to me that IBD declared Wednesday to be a Follow-Through-Day. Since it was only the 2nd day off the bottom this seemed odd to me. I’ve done an extensive series quantifying Follow-Through-Days. IBD’s rules have been fluid over time and sometimes nonsensical based on the evidence. From all appearances they have done very little actual research on their own indicator, and have never shared any verifiable results.

One basic guideline IBD has suggested with Follow-Through-Days is that they should occur between the 4th and 10th day of the beginning of a rally. I examined FTD’s after the 10th day in the February 29, 2008 blog post. At that time I found that FTD’s after day 10 are NOT less reliable as IBD claims. In fact, the small sample was much more reliable.

But what of FTD’s that occur prior to Day 4?

Using the original basic assumptions from the January 14, 2008 study I adjusted the requirement from 4 days (standard) to 2 days (Wednesday’s “FTD”). Below is a quick comparison since 1970. Again, refer to the original basic assumptions for definitions of success and failure of a FTD.

4th Day of Rally Is Earliest Possible FTD – 38 winners and 35 losers.

2nd Day of Rally Is Earliest Possible FTD – 39 winners and 43 losers.

So it appears that allowing FTD’s on day two did identify one additional rally. I looked to see when this additional “success” took place. It was July of 1973. The total rally only lasted 3 weeks. The reason it was “successful” if you entered on the FTD on the 2nd day off the bottom was that the “success” target of a move of twice the size of the distance from the bottom to the FTD was more easily achieved. This “successful” July rally never even went on to break the swing highs of May. Not exactly the kind of winner most traders would be disappointed to miss out on. And while it met the test definition, when looking at a chart it likely isn’t a rally that most traders would even consider successful. Also note that shortening the requirement to 2 days from 4 days triggers 8 more losers.

I don’t agree with many of IBD’s teachings on FTD’s, but in my eyes this particular rule (waiting until day 4) is a very good one. I personally wouldn’t ignore it and am a bit surprised that they did.

My schedule has been different this week and I haven’t been able to get out blogs as easily. Sorry about that. I expect things to return to normal next week.

One study that appeared in the Quantifinder from last night pointed to this post from November of 2008.

https://quantifiableedges.blogspot.com/2008/11/dangers-of-shorting-near-potential.html

The lesson there still holds true.

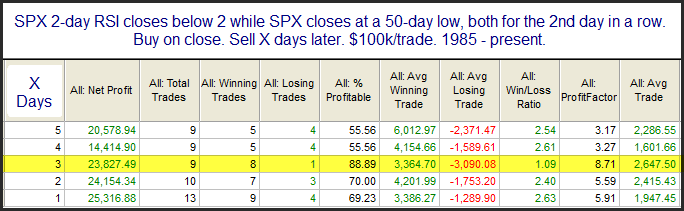

Below is a study from last night’s Subscriber Letter. It looks at when happens when ths SPX has been oversold short-term (via RSI2) and intermediate-term (50-day low).

With 8 of 9 instances trading higher and an average return of 2.65% 3 just 3 days later there appears to be an upside edge. Of course this market has been ignoring oversold conditions for several days now. Still, I’d be more inclined to bet on a short-term bounce than against one.

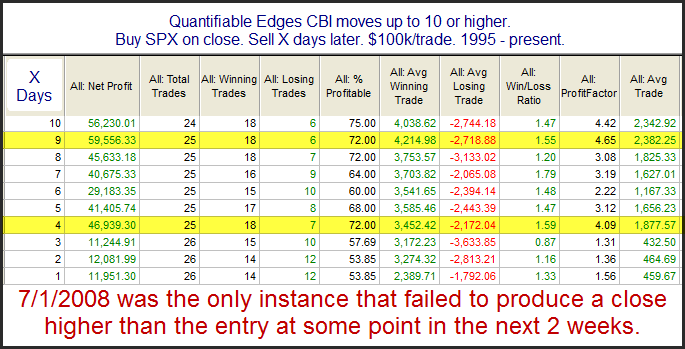

One notable breadth indication that hit an extreme Tuesday is the CBI, which jumped up to 14. I alerted followers of this via Twitter near the close. As I’ve written about and discussed many times in the past, moves to 10 or above have typically been suggestive of a strong bounce within a few days. Below is a simple test that shows results of buying a move up to 10 or higher and then exiting X days later.

More information on the CBI may be found using the CBI label below. Also, I recently updated the Catapult and CBI presentation in the members section of the website. If you would like to see the presentation or see the trade triggers that have pushed the CBI up to 14, you may take a free trial. (If you are already in the system but haven’t trialed yet in 2010, just drop me a note and I’ll set you up with one.)

A little over a week ago I showed a study that examined large gaps up from high levels. The results were very compelling and suggested a strong downside edge. Today we are presented with a similar situation in the opposite direction. So this morning I ran some tests that looked at large gaps down from a low area. Below is one example typical of what I saw:

Perhaps a mild upside edge could be found, but certainly nothing as compelling as last week’s study. Results were volatile as well, with the average intraday drawdown over 1.6% and the average run-up over 2%.

Below I tightened the requirements to a 1% gap and showed all instances. Results were similar – just with fewer instances.

Bottom line is there may be a slight upside edge, but the direction is certainly no layup. No matter the direction be prepared for some volatile action today.

It was just a little over a week ago that I was examining what occurs after the market posts 2 90% Up Days in a 1-week period. The results appeared quite bullish. Thursday we saw the 2nd 90% down day in the last 3 days. I stretched the requirement out to 1 week and took a look.

For the short-term at least, such negative breadth appears to suggest a bounce.

A good question a reader sent to me yesterday was to explain how futures or options may be used to predict Fed rates. A great source to gain a better understanding of this subject is the Cleveland Fed’s website. The link below is to their FAQ’s page:

https://www.clevelandfed.org/research/data/fedfunds/faq.cfm

Questions 4 and 8 deal directly with this topic. Copy and pasting the information found there is a bit difficult since they use tables in the description. Should you have interest in how it is all done, simply click the above link and read the answers to questions 4 and 8.

Of course gaining a better understanding of how futures may be used to gauge expectations doesn’t mean you want to actually do the calculations. Fortunately, they do them for you. The link below is updated daily and shows estimates for meeting outcomes.

https://www.clevelandfed.org/research/data/fedfunds/

Currently the estimates are suggesting there is virtually no chance of a rate increase tomorrow.

Of course even if you know what the Fed is going to do with rates, that doesn’t tell you any probabilities or edges related to market reaction and behavior on or around these meetings. For that information, you’ll need to read “The Quantifiable Edges Guide to Fed Days“. The next Fed Day is tomorrow, June 23rd. The guide is available in ebook or paperback. If you would prefer the paperback, but want to read it tonight, just email your purchase receipt before tomorrow’s meeting and I’ll send you the ebook version.

Edit: Jeff Pietsch of Market Rewind in the comments section provided a link to a tool from the CME that predicts rates. Below is a lnk to the tool:

https://www.cmegroup.com/trading/interest-rates/fed-funds.html