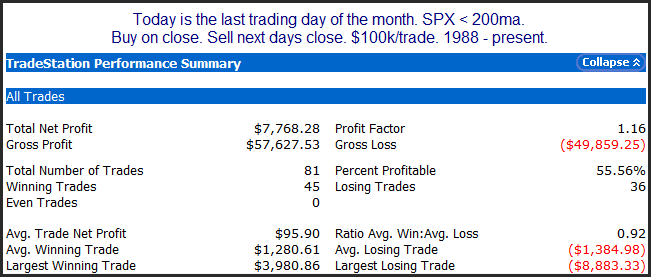

Veterans Day Performance

Veterans Day is one of the few US holidays when the bond market is closed and the stock market is open. Columbus Day is another. But while Columbus Day has exhibited some quantifiable edges, Veterans Day has not. Veterans Day is celebrated on November 11th (or the closest weekday to November 11th) each year. For a brief period from 1971 – 1977 it was celebrated on the 4th Friday of October. Below is a profit curve that shows how Veterans Day has performed over the years.

While for a good long while it appeared Veterans Day may provide an upside edge, the curve topped out in 1992. Since then it has been mostly lower. Happy Veterans Day and thanks to all veterans!