I wanted to briefly discuss the Vegas Traders Expo I attended last week. I enjoyed the Expo greatly. While there was a good number of unsubstantiated claims by certain speakers, I was pleased to see that several speakers took the time to quantify their methods. Two that come to mind were Larry Connors and Buff Dormeier.

Larry discussed some of his TradingMarkets work.

Buff discussed his Volume Price Confirmation Index (VPCI), which he won the Charles H. Dow award for in 2007. For those who may not have read Mr. Dormeier’s paper I would suggest it. It may be found using the link below:

https://www.mta.org/eweb/docs/2007DowAward.pdf

In fact, all past Dow Award winning papers back to 1994 may be found here:

https://www.mta.org/EWEB/dynamicpage.aspx?webcode=charlesdowaward

Other traders whose work I respect greatly and had a chance to meet and talk with at the expo include:

Scott Andrews of Master the Gap. Scott’s focus is trading the opening gap – primarily in the S&P futures. He uses statistics and backtesting to develop his techniques.

Tim Bourquin of TraderInterviews.com – a unique site that interviews traders to provide insights into how they make money.

Dave Mabe of Stocktickr. The Stocktickr product helps traders to track, segment and journal their trades. I strongly believe it’s important to understand what’s working and what isn’t among a traders strategies and this product seems to do a nice job of assisting with that.

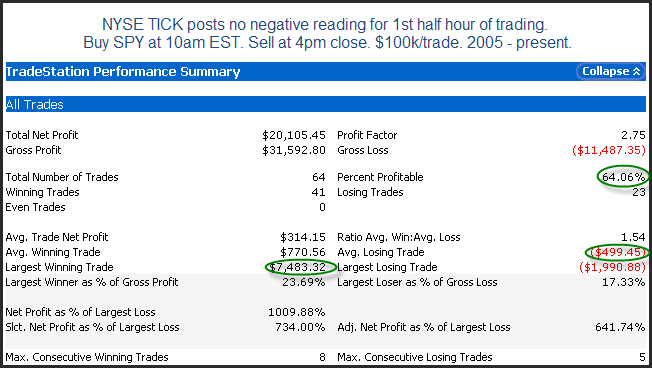

Corey Rosenbloom of Afraid to Trade. Corey focuses on intraday trading and technical analysis. He looks for trade confirmation using several techniques including Fibonacci, Eliot Wave, and tick analysis.

I also enjoyed meeting and speaking with several Quantifiable Edges readers and subscribers.