This past week I had the pleasure of interacting with Tom McClellan of McClellan Financial Publications (https://www.mcoscillator.com/). Tom shared a study with me that supported some breadth related studies from the Quantifiable Edges Subscriber Letter that I’d been discussing the last few weeks.

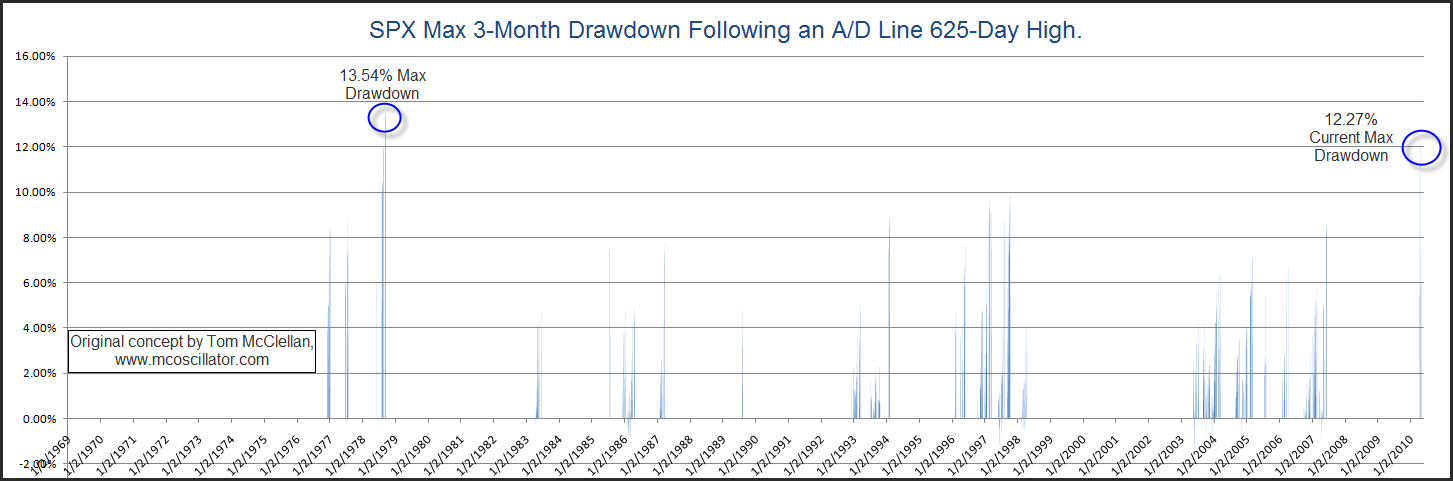

Tom’s study looked to measure market risk when the A/D line was making new highs. To accomplish this he examined any time the Advance/Decline line made a 3-year high and then looked forward 3 months to see what the max drawdown was in the SPX. The SPX has not managed to make a 3-year high in the A/D line recently. It DID make a 2 ½ year high about a month ago though. So I re-ran the study with Tradestation data (which should be very similar) and used a requirement of a 2 ½ year high instead of 3 years.

Note: A full year typically contains about 252 trading days. For purposes of this test I rounded that down to 250 and multiplied by 2.5 to get 625 trading days. To estimate 3 months I used a 63-day period. Also note that the flat spots on the chart are times when the high A/D condition is not met.

(click chart to enlarge)

As you can see above, since 1970 there has only been one instance that saw a larger drawdown over the following 3 months than we’ve already seen this past month. Other corrections were generally capped at between an 8% – 10% decline. This doesn’t mean we can’t drop precipitously from here. The market has demonstrated several times in the past few years that it is completely capable of breaking records. It does show that we’ve reached an area where risk has pretty much maxed out in the past under similar conditions – at least temporarily.