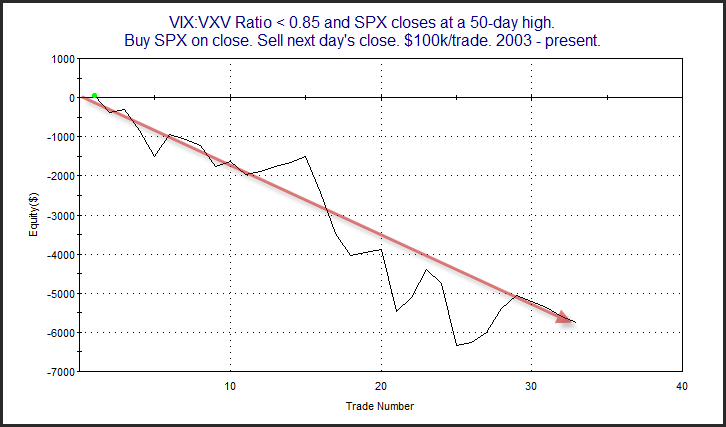

Examining the VIX:VXV ratio is a concept I first heard from Bill Luby at VIX & More. The VIX is a measure of short-term (30-day) volatility expectation and the VXV measures intermediate-term (93 day) volatility expectations. The ratio right now is quite low – a little below 0.85. This means that short-term volatility expectations are substantially below intermediate-term volatility expectations. When readings this low coincide with 50-day SPX highs it suggests a possible bearish edge for the next day. This was demonstrated in a study that the Quantifinder identified yesterday afternoon. It last appeared in the 1/13/11 subscriber letter. I updated it last night. Below is an equity curve showing a 1-day holding period for this setup.