For much of last week I was at the National Association of Active Investment Managers (NAAIM) Uncommon Knowledge conference. NAAIM is a terrific organization that I have become more involved with over the years.

NAAIM has published its “NAAIM Exposure Index” since 2006. I did some research a few years ago on the index to determine whether the numbers might be valuable as part of a model. I found that 1) strongly oversold readings could be indicative that the market is so oversold it is ready to rally, 2) strongly overbought readings are not a contrarian indicator. In fact they often suggest strong momentum that is likely to continue. I had a discussion with some NAAIM members a few weeks back. The topic was the Exposure Index: who used it, what they used it for, and where was the actual value in it?

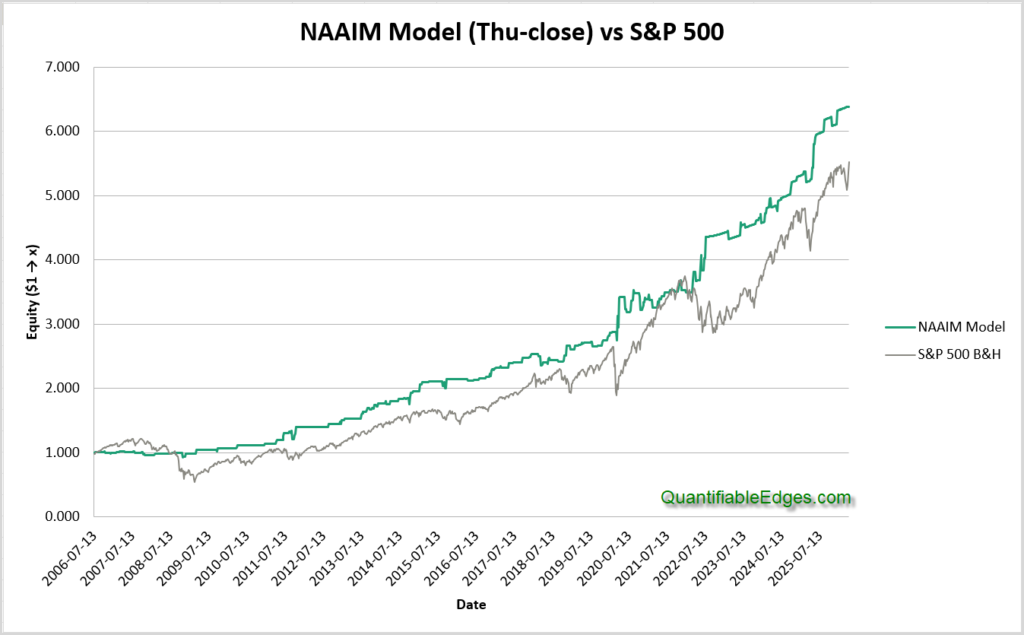

So I decided to revisit my old research and see if I could create a model based on those concepts that could demonstrate the value that the index provides. Results came out better than anticipated. Below is a look at the profit curve of the model versus the S&P 500.

The NAAIM Exposure Index is released each week during market hours on Thursday. So the model trades at the close every Thursday afternoon. (Thanksgiving and other holidays will sometimes bump it forward one day.) There are three setups that will cause the model to go long.

This week’s reading is among the bottom 10% of readings seen over the last 52 weeks (one year). Additionally, it is not lower than last week’s reading. Essentially this is looking for a strongly oversold reading, but not looking to catch a falling knife. So we want to see the Exposure Index near or slightly above where it was the week before.

This week’s reading is at least 80 and it has risen at least 15 points over the last four weeks. This is looking for strong and growing enthusiasm.

This week’s reading is at least 100. As it turns out, when you have a bunch of smart investment managers getting leveraged, there is a good chance that they are right and that there are market gains ahead.

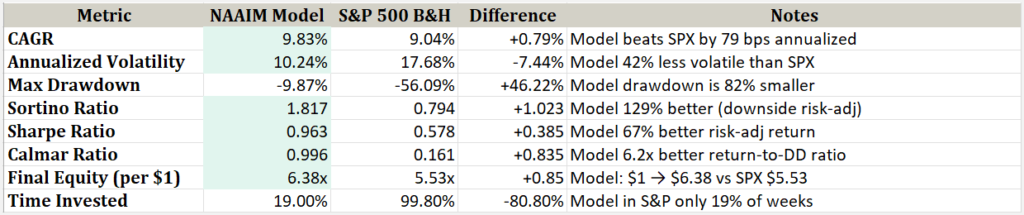

If any one of the above is true, the model will go (or remain) long 150% SPX at the close on Thursday, and will remain long at least until the following Thursday when the new number is published. Below is a stats table summarizing the results.

The numbers here compare very favorably to the SPX. Leverage when there is an edge and cash when there is not. As you can see the model’s only invested 19% of the time. That is a big risk reducer. One thing to note is the Max Drawdown. It is shown as less than 10% in the table above. But that is partially because this model is just using weekly closing numbers. I created a version in Realtest that uses daily pricing. And thanks to March 2020, the max drawdown reached 25% using daily bars. (Still less than half that of the S&P 500.)

Is this a model I would actually trade? No. I don’t think I’d trade any model where I had to hold for a full week based solely on survey results. Of course the fact that it is built solely on survey results, and does not take into account price, or trend, or volume, or breadth, or anything else, is what really demonstrates the value of the NAAIM Exposure Index. And that was kind of the whole point. Trading solely on the index may be overenthusiastic but utilizing it as one input within a larger model seems completely reasonable and could very possibly strengthen it.

I have the model available in both Excel and Realtest format. If you have a username and password at Quantifiable Edges, then you can download the model from the Other Code and Spreadsheets page. If you don’t have a log-in, you can get one by simply signing up for a free trial! And if you don’t want a free trial right now, then just join our email list and you will receive a copy. Easy as pie.

Disclaimer: The performance shown above is hypothetical and does not represent an actual trading account. Results were generated frictionlessly, meaning they do not include commissions, slippage, or other costs that would be incurred in live trading. Past performance, actual or hypothetical, is no guarantee of future results.