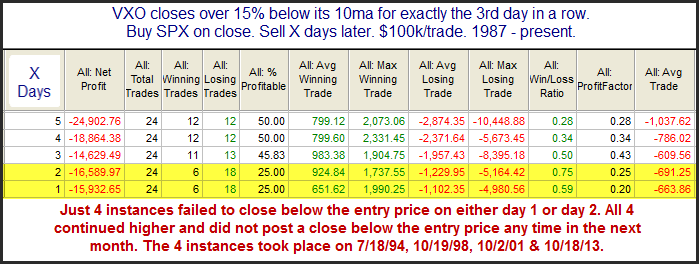

Both the VIX and the VXO have been extended to the downside in recent days. Such stretches suggest a collapse in fear among investors. The study below was last seen in the 12/27/13 blog. It looks for stretches of 15% or more that have persisted for three days.

Based on the stats table there appears to be a downside inclination. The note at the bottom of the study is especially interesting. Nearly every case has experienced an almost immediate pullback, but those that didn’t went without pulling back for a long time.

Want research like this delivered directly to your inbox on a timely basis? Sign up for the Quantifiable Edges Email List.

Rob Hanna is the founder of Quantifiable Edges, a quantitative market research service he has run since 2008. His research focuses on statistical analysis of U.S. equity markets, including studies on FOMC patterns, VIX dynamics, seasonal effects, gap behavior, market breadth, and other quantitative edges. In 2009 he published "The Quantifiable Edges Guide to Fed Days," available on Amazon. He was named the 2024 recipient of the National Association of Active Investment Managers (NAAIM) Founders Award and currently serves on the NAAIM Board of Directors. His articles have appeared in several trading and investment publications, and he has been a guest on numerous trading podcasts. Rob has been a featured speaker at annual conferences for the CMT Association (formerly Market Technicians Association), the American Association of Professional Technical Analysts (AAPTA), and NAAIM. He ran a private investment partnership from 2001 through 2019 before joining Capital Advisors 360 as an investment advisor representative, where he trades quantitative and volatility-based models for clients.. Follow him on Twitter / Facebook.